Digital payments and credit card use is growing. This means more merchant accounts are being opened. A merchant account is a type of bank account that allows businesses to accept credit and debit card payments. In this article, we’ll take a closer look at how a merchant account works and why it’s essential for businesses.

What is a merchant account?

A merchant account is a type of bank account that allows businesses to accept payments from customers through various payment methods, such as credit cards, debit cards, or mobile payments. It acts as an intermediary between the business, the customer, and the financial institution.

When a customer makes a purchase, the funds are first handled to the merchant account. From there, the funds are settled and deposited into the business’s regular bank account. Merchant accounts typically involve agreements with payment processors or acquiring banks to facilitate the transaction process and ensure the secure transfer of funds.

How does a merchant account work?

To accept electronic payments, a business needs to open a merchant account with a merchant account provider. This can be a payment processor like Clearly Payments where you get a dedicated merchant account or a third-party payment processor like Square where you get a shared merchant account. You can read more about the difference between a merchant account and a third-party processor. The merchant account provider will set up the business with a unique merchant ID, which is used to identify the business when processing transactions.

When a customer makes a purchase with a credit or debit card, the transaction is processed through the merchant account provider’s payment gateway. The payment gateway is a software application that connects the business’s website or point-of-sale (POS) system to the merchant account provider’s processing network. It encrypts the customer’s payment information and sends it securely to the merchant account provider for processing.

The merchant account provider then verifies the transaction and sends a request to the customer’s bank or card issuer for authorization. If the transaction is approved, the funds are transferred from the customer’s account to the merchant account. The merchant account provider then deducts any fees, such as interchange fees and processing fees, before transferring the remaining funds to the business’s bank account.

The categories of merchant accounts

Yes, there are different types of merchant accounts that cater to specific types of businesses and their payment processing needs. They are typically based on their MCC (merchant category code). Here are some of the most common types of merchant accounts:

Retail merchant accounts: This type of merchant account is best suited for businesses that operate in a physical storefront or retail location, where transactions are processed through a credit card payment terminal or point-of-sale (POS) system.

eCommerce merchant accounts: eCommerce merchant accounts are designed for businesses that primarily sell goods or services online. These accounts typically integrate with payment gateways and shopping cart software to facilitate online transactions.

MOTO merchant accounts: MOTO (Mail Order/Telephone Order) merchant accounts are used by businesses that primarily accept payments over the phone or through the mail.

High-risk merchant accounts: Some businesses are considered high-risk due to their industry, business model, or credit history. High-risk merchant accounts are designed for these types of businesses and typically come with higher fees and stricter underwriting requirements.

International merchant accounts: International merchant accounts allow businesses to accept payments in foreign currencies and cater to businesses that operate globally.

Aggregator merchant accounts: Aggregator merchant accounts are designed for small businesses and start-ups that do not meet the underwriting requirements of traditional merchant accounts. These are generally for businesses that have less than $100,000 per year in credit card processing. These accounts typically come with higher fees but have lower barriers to entry. Examples that provide aggregator merchant accounts are Square, Stripe, and PayPal.

It’s important for businesses to select the type of merchant account that best suits their payment processing needs. Businesses should consider factors such as their industry, payment volume, and transaction types when selecting a merchant account provider.

The flow of a transaction for a merchant account

A transaction with a merchant account involves a series of interactions between a business and its customers to facilitate payment for products or services. The merchant account serves as a financial intermediary, allowing businesses to accept various payment methods such as credit cards or mobile payments.

This enables the smooth transfer of funds from the customer’s account to the merchant’s account, ensuring a secure and efficient transaction process.

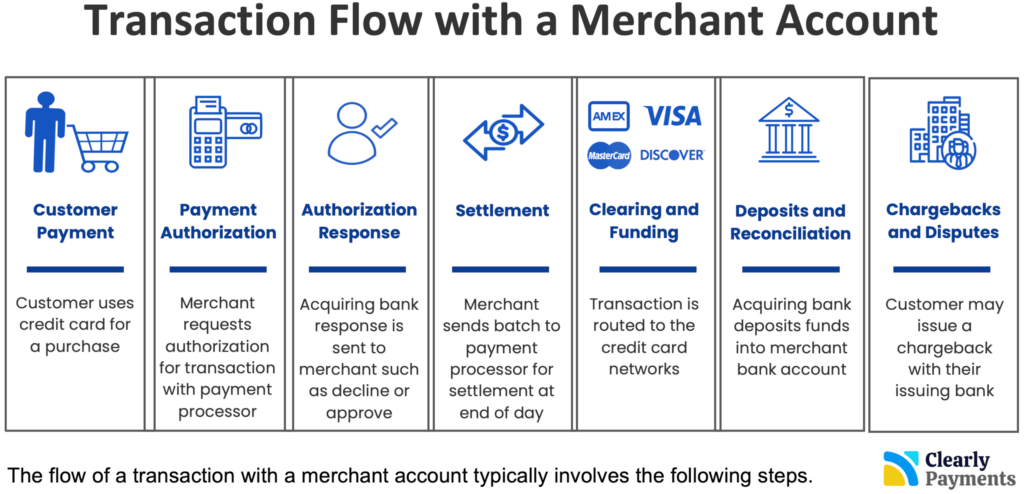

The flow of a transaction with a merchant account typically involves the following steps:

Customer initiates the transaction: The customer decides to make a purchase from the merchant, either in-person or online, with a credit card.

Payment authorization: The merchant requests authorization for the transaction from the payment processor or acquiring bank. This involves verifying the customer’s payment details and ensuring there are sufficient funds or credit available.

Authorization response: The payment processor or acquiring bank sends an authorization response to the merchant, indicating whether the transaction is approved or declined. If approved, the merchant can proceed with fulfilling the order.

Settlement: Once the order is fulfilled, the merchant batches and submits the authorized transactions to the payment processor for settlement. The payment processor verifies the transactions and transfers the funds from the customer’s account to the merchant’s account.

Clearing and funding: The payment processor routes the transactions to the relevant credit card networks (such as Visa or Mastercard) for clearing. The card networks facilitate the transfer of funds between the customer’s issuing bank and the merchant’s acquiring bank.

Deposits and reconciliation: The acquiring bank deposits the funds into the merchant’s designated bank account, typically in a batch format. The merchant reconciles the settled transactions against their own records to ensure accuracy.

Chargebacks and disputes: In case of any customer disputes or chargebacks, where the customer requests a refund through their card issuer, the merchant may receive a notification and have the opportunity to dispute the chargeback by providing evidence.

It’s important to note that the specific flow and timelines can vary depending on the payment processor, acquiring bank, and the merchant’s agreement with their service providers. Additionally, online transactions may involve additional security measures, such as 3D Secure authentication, to mitigate fraud risks.

Why is a merchant account important for businesses?

Accepting electronic payments is essential for businesses to remain competitive in today’s market. With more consumers choosing to pay with credit and debit cards over cash, businesses that don’t accept these payment methods risk losing customers to their competitors. A merchant account also provides businesses with several other benefits, such as:

- Increased sales: Accepting electronic payments can increase sales by making it easier for customers to make purchases.

- Improved cash flow: Electronic payments are typically processed faster than checks, which can improve a business’s cash flow.

- Enhanced security: Electronic payments are more secure than cash and checks, as they are encrypted and protected by fraud detection measures.

- Access to online sales: A merchant account allows businesses to accept payments online, which can open up new sales channels.

A merchant account is a critical tool for businesses that want to accept electronic payments. By providing a secure and reliable payment processing solution, a merchant account can help businesses increase sales, improve cash flow, and enhance customer satisfaction.

Where to get the best merchant account

When searching for the best merchant account, consider factors such as reliability, payment processing options, competitive pricing, integration capabilities, security measures, customer support, scalability, and favourable contract terms. Research and compare providers, read reviews, and seek advice from industry experts to find the merchant account that offers a solid reputation, comprehensive features, and excellent value.

Get the best merchant account with Clearly Payments

- Lowest-cost processing in the industry

- Fund transfers in less than one day

- A full set of payment products to accept payment anytime, anywhere

- World-class customer service