There is a cost for merchants to accept credit cards. You most likely already know this. Payment processors provide the software and hardware, services around fund transfers, and customer support. In addition, payment processors take risk for giving credit to merchants during the process of accepting credit cards.

One example scenario of the type of risk that payment processors take is the following. Imagine you are an online merchant that sells $100,000 of jewelry. Within 24 hours, the customer’s money is deposited into your bank account. If you take that $100,000 and don’t ship the jewelry to the customers for whatever reason, there is a problem. The customers are going to complain about the charge to their banks and they will get their money back. If the business won’t give the $100,000 back, the payment processor is on the hook to pay it back. That’s the risk that payment processors take. And that’s also the reason payment processors sometimes put holds on funds and also why they have an underwriting process.

There are typically three fees that merchants pay

The fees that merchants pay for credit card processing can be complex. If you see a processor that advertises zero fees, don’t believe them. It’s not true.

Aggregators (like Stripe, Square, and PayPal) generally have a simple percentage fee and a transaction fee. Merchant account providers (like Clearly Payments and Moneris) tend to have a more detailed breakdown of fees and a monthly fee, making them seem more complex. The benefit of merchant accounts is that you can customize the pricing of each of the fees to match your business. The nice thing about aggregator accounts is that there tend to be only two fees. Overall, the main types of fees a merchant will pay are:

• A percentage fee that may range from 1.8% to 3% or even more,

• A transaction fee that may range from $0.04 to $0.40, and

• A fixed monthly charge that may range from $0 to $50.

In the end, the best way to compare aggregator vs merchant account fees is to contrast the effective rate. This means taking the total fees and dividing them by your total revenue. This gives you a percentage that is your effective rate.

The fees and economics of aggregators vs merchant account providers

The makeup of your fee structure has a drastic impact on the fees you end up paying. Merchant account providers and aggregators have very different pricing models. Aggregator (i.e. Square) pricing models work best for small businesses and merchant account (i.e. Clearly Payments) pricing models work best for medium to large businesses.

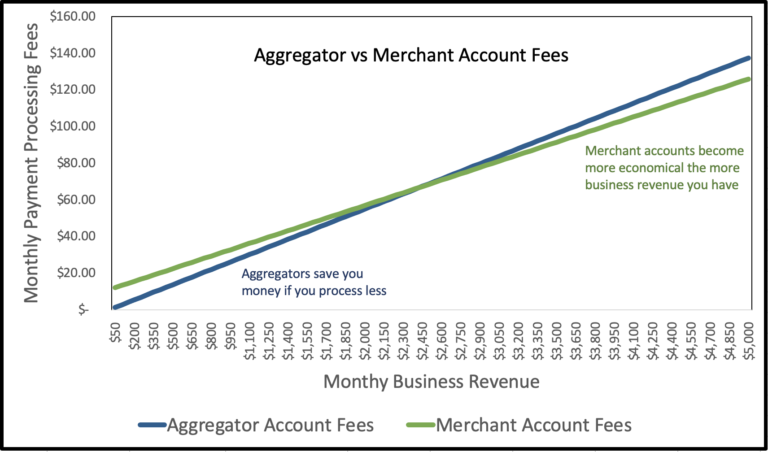

The below chart explains the basics of how to compare the effective rates. In the end, you’ll see that aggregator pricing is lower if there is a small amount of processing. The larger your processing amount, the more it starts to make sense to sign up for a merchant account. This is why aggregator accounts are generally better for smaller businesses.

Aggregators have a higher percentage fee (i.e. 2.9%) and a higher transaction fee (i.e. $0.30), but no monthly fee. Merchant accounts tend to have a lower percentage fee (i.e. 2.3%) and a lower transaction fee (i.e. $0.08), but have a monthly fee (i.e. $13). We recommend thinking about upgrading from an aggregator to a full merchant account when you hit the level of around $5000 per month in processing.

Other economic considerations of aggregators vs merchant accounts

Sometimes there are different fees depending on how you accept a credit card payment. In Square, for example, there is a standard 2.65% and $0.10 fee for general processing, however, the rate jumps to 3.4% and $0.15 if you have a saved card on file or you type in credit card numbers. This has a material impact on the economics, especially when you get to $5000 or more in processing per month.

The good merchant account providers charge on a cost-plus basis. This means they charge a small percentage on top of the interchange fees that the banks charge. This gets you the lowest price, regardless of accepting credit cards by swipe, keyed-in, tap, or any other method.

Summary and recommendation for a payment account

There are pros and cons of merchant accounts vs aggregators. The answer is “it depends”. In summary, use an aggregator if you process less than $10,000 per month. If you process more than $10,000 per month, get a merchant account.

If you want hands-on support or you have things outside the norm like high transaction amounts (i.e. $5000+) or conduct many transactions per month (i.e. 5,000+ transactions), you should likely go with a merchant account.