Every day, millions of online purchases move through a global payments infrastructure that most consumers never see. A customer clicks “Buy Now”, receives an approval message within seconds, and assumes the transaction is complete.

In reality, that single payment triggers a complex chain of financial institutions, technology providers, security systems, and regulatory processes that work together to move money safely from one party to another.

For merchants, understanding how these economics work is increasingly important. Payment acceptance is often one of the largest operating expenses associated with e-commerce, yet many businesses only see a single processing fee on their monthly statement.

This report examines the typical economics behind a $100 online credit card transaction in North America and explores where that money actually goes.

The Journey of a $100 Transaction

Consider a customer purchasing a product online for $100 using a rewards credit card.

The transaction appears simple from the customer’s perspective, but behind the scenes several organizations participate:

- The customer and their issuing bank

- The merchant

- The payment processor

- The acquiring bank

- The card network

- Fraud and security providers

- Various infrastructure and software providers

Within seconds, authorization requests travel through multiple systems before the transaction is approved and the merchant can fulfill the order.

While every payment is unique, the economic structure is remarkably consistent across the industry.

Breaking Down a Typical $100 Online Purchase

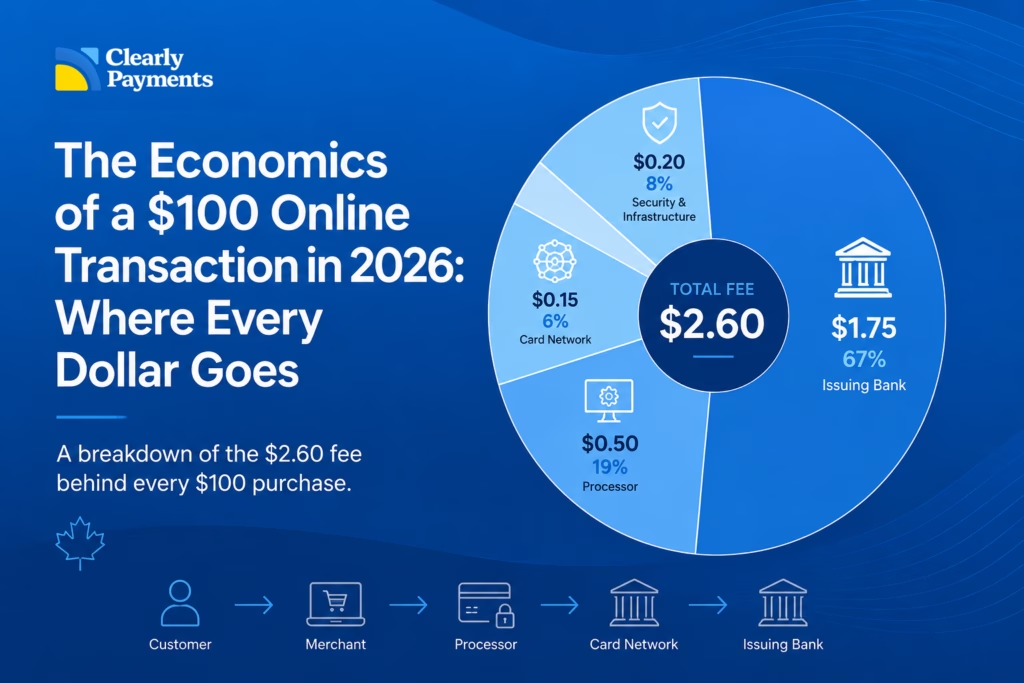

For a typical North American e-commerce transaction, total payment acceptance costs often range between 2.2% and 3.0% of the transaction value.

Using a representative transaction costing approximately 2.6%, the economics might look something like this:

Recipient | Approximate Amount |

Merchant Receives | $97.40 |

Issuing Bank | $1.75 |

Card Network | $0.15 |

Payment Processor | $0.50 |

Infrastructure & Security Providers | $0.20 |

Total Payment Costs | $2.60 |

The most surprising aspect for many merchants is that the majority of payment costs do not go to the payment processor.

In most cases, issuing banks receive the largest share of the economics through interchange fees.

Why Issuing Banks Receive the Largest Share

The issuing bank is the financial institution that provided the customer’s credit card.

When consumers use credit cards, issuing banks assume significant responsibilities and risks. They extend credit, fund rewards programs, absorb certain fraud losses, manage disputes, operate customer service departments, and handle collections.

These activities are largely funded through interchange revenue.

As premium rewards cards have become more common, interchange costs have generally increased. Consumers enjoy airline miles, cash-back rewards, travel benefits, and purchase protection programs, but these benefits must ultimately be funded somewhere within the payment ecosystem.

For many online transactions, interchange represents approximately 65% to 80% of the total payment acceptance cost.

This means that when a merchant pays $2.60 to accept a $100 payment, roughly $1.75 may be allocated to the issuing bank.

The Role of Visa and Mastercard

Card networks act as the infrastructure layer connecting thousands of financial institutions around the world.

When a customer makes a purchase, card networks facilitate communication between the merchant’s acquiring bank and the customer’s issuing bank.

They establish operating rules, security standards, settlement procedures, and dispute resolution frameworks that allow electronic payments to function at global scale.

Although Visa and Mastercard are often the most visible brands in the payment process, their direct share of transaction economics is generally much smaller than many merchants assume.

Network assessment and processing fees typically represent only a small percentage of the total acceptance cost.

Yet without these networks, modern electronic commerce would be significantly more difficult and fragmented.

What Payment Processors Actually Do

Many merchants believe their payment processor keeps the majority of the fees they pay.

In reality, processors typically retain only a fraction of the overall transaction cost after passing through interchange and network fees.

Modern processors perform a wide range of functions, including:

- Merchant underwriting

- Risk management

- Payment gateway services

- Settlement and funding

- PCI compliance support

- Chargeback management

- Reporting and analytics

- Technical integrations

- Customer support

Processors also invest heavily in infrastructure to maintain high availability, security, and transaction performance.

For many providers, profit margins are significantly lower than merchants often assume because a substantial portion of every transaction fee is remitted to banks and card networks.

The Growing Cost of Fraud

One of the least visible expenses within the payment ecosystem is fraud prevention.

As e-commerce continues to grow, fraud has become increasingly sophisticated. Merchants now face challenges ranging from stolen card usage and account takeover attacks to synthetic identity fraud and automated bot activity.

The true cost of fraud extends far beyond the original transaction amount. Consider a fraudulent $100 purchase:

- Inventory may be lost

- Shipping costs are incurred

- Payment processing fees may not be recoverable

- Chargeback fees may apply

- Customer service resources are consumed

As a result, a fraudulent $100 transaction can easily create total losses exceeding $150.

To combat these risks, merchants and payment providers increasingly invest in machine learning systems, device intelligence, behavioral analytics, tokenization, and advanced fraud screening tools.

These investments help protect merchants but also contribute to the overall economics of payment acceptance.

Comparing Different Payment Methods

Not all payment methods carry the same cost structure. Credit cards remain the dominant payment method for online commerce because they offer convenience, rewards, fraud protection, and broad consumer adoption. However, alternative payment methods can significantly alter transaction economics.

Payment Method | Typical Cost Range |

Debit Card | 0.5% to 1.5% |

Credit Card | 2.0% to 3.5% |

ACH / EFT | Fixed fee or low percentage |

Bank Transfer | Often significantly lower |

Digital Wallets | Similar to underlying funding source |

In most cases, digital wallets such as Apple Pay or Google Pay do not eliminate card costs because they are typically funded by the same underlying credit or debit card networks.

What Merchants Can Actually Control

Many payment costs are determined by factors outside a merchant’s control.

Merchants generally cannot negotiate:

- Interchange schedules

- Network assessment fees

- Card reward structures

- Regulatory requirements

However, businesses can influence several important variables:

Payment Mix

Encouraging lower-cost payment methods can reduce overall acceptance expenses.

Fraud Rates

Lower fraud rates often result in fewer chargebacks and lower risk-related costs.

Authorization Performance

Improving checkout experiences and reducing failed transactions can increase revenue without increasing marketing spend.

Processor Markup

While interchange and network fees are largely fixed, processor markups vary considerably between providers.

Operational Efficiency

Consolidating systems, reducing manual processes, and improving reporting can lower the total cost of managing payments.

The most effective payment optimization strategies focus on these controllable factors rather than chasing unrealistic reductions in interchange costs.

Looking Ahead

The economics of payments continue to evolve. Artificial intelligence is transforming fraud detection. Real-time payment systems are expanding globally. Open banking initiatives are creating new account-to-account payment options. Tokenization is improving security while reducing fraud exposure.

At the same time, digital commerce continues to grow, increasing the importance of reliable and secure payment infrastructure.

Over the next decade, merchants may see greater adoption of real-time bank payments, expanded use of digital identity systems, and even autonomous AI agents capable of initiating purchases on behalf of consumers and businesses.

Despite these changes, one principle is likely to remain constant: moving money securely is more complex than it appears.

Conclusion

A $100 online transaction may look simple from the outside, but it activates an extensive ecosystem of banks, payment networks, processors, security providers, and technology platforms.

Of a typical $100 online purchase, the merchant might receive approximately $97.40 after payment acceptance costs. The remaining amount is distributed across the organizations responsible for extending credit, preventing fraud, operating global networks, and ensuring transactions move securely and reliably around the world.

For merchants, understanding these economics provides valuable context for evaluating payment providers, managing costs, and making informed decisions about payment strategy.

The payment processor is only one participant in a much larger system, and appreciating the role of each participant helps explain why payment acceptance costs exist in the first place.