When a customer taps, inserts, or enters a credit card online, the transaction appears almost instantaneous. A receipt is generated, funds begin moving, and the sale is complete.

Behind that simple experience, however, exists one of the most sophisticated financial systems ever built. Every card payment triggers a series of interactions between issuing banks, acquiring banks, payment processors, card networks, fraud systems, and settlement infrastructure.

At the center of this ecosystem sits a charge known as the interchange fee.

Interchange fees represent the largest component of card acceptance costs for most merchants, yet they remain one of the least understood aspects of payment processing. Businesses often focus on the rate charged by their processor while overlooking the fact that the majority of the cost is determined by interchange.

Understanding how interchange works is essential for any business that accepts card payments because it explains where processing costs originate, why rates vary so dramatically, and how merchants can optimize their payment economics.

What Is an Interchange Fee?

An interchange fee is a transaction fee paid from the merchant’s acquiring bank to the customer’s issuing bank whenever a card payment is processed. These fees are established by the major card networks and are designed to compensate issuing banks for providing credit, managing accounts, funding rewards programs, and assuming fraud and credit risk.

In simple terms:

- The customer uses a card issued by Bank A.

- The merchant processes the transaction through Acquirer B.

- Acquirer B sends a portion of the transaction value to Bank A.

- That payment is the interchange fee.

For most merchants, interchange accounts for approximately 70% to 90% of the total cost of card acceptance.

Many business owners assume their processor determines the entire transaction fee. In reality, processors often have limited control over interchange itself because the rates are largely set by the card networks.

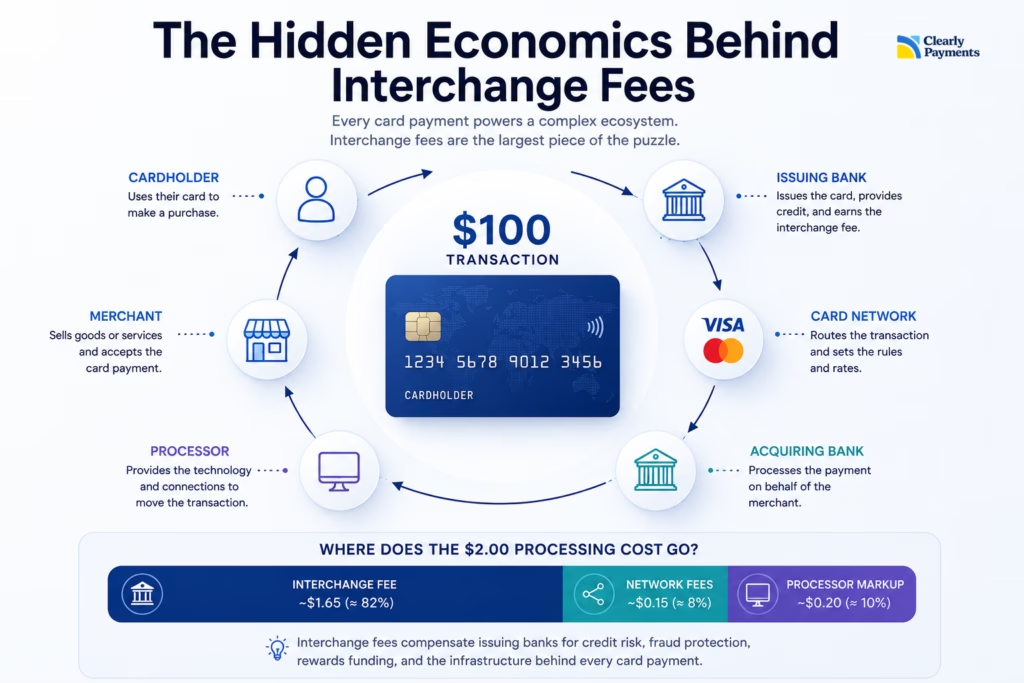

Following a $100 Transaction

Consider a typical $100 credit card purchase.

| Component | Example Amount |

|---|---|

| Sale Amount | $100.00 |

| Interchange Fee | $1.65 |

| Network Assessment | $0.15 |

| Processor Markup | $0.20 |

| Total Processing Cost | $2.00 |

| Merchant Receives | $98.00 |

Although exact values vary, this example highlights a critical reality: the processor may only retain a small fraction of the total fee while interchange represents the majority of the cost.

This is why two processors can offer dramatically different pricing models while still having nearly identical underlying interchange costs.

Who Gets Paid?

A card transaction involves multiple participants.

| Participant | Role | Revenue Source |

| Cardholder | Makes purchase | Rewards and convenience |

| Merchant | Sells goods/services | Revenue from sale |

| Issuing Bank | Provides card to customer | Interchange revenue |

| Acquiring Bank | Processes merchant transactions | Acquiring fees |

| Card Network | Routes transactions | Assessments and network fees |

| Payment Processor | Provides payment infrastructure | Processing markup |

The issuing bank is typically the largest beneficiary of interchange fees.

This economic structure exists because issuing banks assume substantial responsibilities. They extend credit, absorb fraud losses, finance rewards programs, manage cardholder relationships, maintain compliance systems, and fund the infrastructure required to authorize billions of transactions annually.

Interchange Is Really a Risk-Pricing System

Many merchants think interchange is simply a fee. In reality, interchange is often a pricing mechanism for risk. Higher-risk transactions generally attract higher interchange:

| Transaction Type | Relative Risk |

|---|---|

| Chip + PIN | Low |

| Contactless | Low |

| Online Purchase | Medium |

| Manually Keyed | High |

| Travel Industry | Higher |

The hidden economics are that interchange doesn’t just move money. It distributes fraud and credit risk across the payments ecosystem.

Why Some Transactions Cost More Than Others

One of the most confusing aspects of interchange is that there is no single interchange rate.

Thousands of interchange categories exist.

The cost of a transaction can vary based on:

| Factor | Impact on Cost |

| Credit vs Debit | Credit generally costs more |

| Rewards Card | Usually higher interchange |

| Business Card | Often higher than consumer cards |

| In-Person vs Online | Online generally higher risk |

| Industry Type | Certain industries qualify for special rates |

| Transaction Size | Can affect economics |

| Settlement Speed | Delays may increase cost |

| Security Data Submitted | Better data can lower rates |

A premium rewards credit card used online can cost several times more than a regulated debit card used in person.

The merchant sees both transactions as simple card payments, but the economics behind them are entirely different.

The Scale of the Interchange Economy

| Metric | Value |

| Debit & Prepaid Transactions | 100.7 billion |

| Total Transaction Value | $4.7 trillion |

| Annual Interchange Revenue | $34.1 billion |

| Average Annual Growth Since 2021 | 3.9% |

The Rewards Arms Race: Why Merchants Help Fund Your Free Flights

Most consumers believe airline miles, cash back, and premium card perks are funded by banks. The reality is more complicated.

Over the last two decades, banks have competed aggressively for affluent cardholders by offering richer rewards programs. To support those rewards, issuers rely heavily on interchange revenue generated every time a card is used.

This has created what many industry observers call a rewards arms race. Banks compete to offer more points, more cash back, and more perks. Consumers increasingly choose premium rewards cards. Merchants then face higher acceptance costs because premium cards often carry significantly higher interchange rates than basic cards.

The hidden economic effect is that rewards are not funded solely by banks. They are partially funded by the millions of businesses that accept those cards every day.

| $100 Purchase | Approximate Merchant Cost |

|---|---|

| Debit Card | $0.25 – $0.50 |

| Standard Credit Card | $1.50 – $2.00 |

| Premium Rewards Card | $2.50 – $3.50+ |

For merchants, the sale looks identical. The economics behind it are not.

The Merchant's Dilemma: Why Businesses Benefit From the System They Complain About

Merchants often view interchange as a cost. Yet the same payment system that generates interchange fees also helps drive higher sales.

Research consistently shows consumers spend more when using cards than when using cash. Credit cards reduce purchase friction, increase convenience, and allow consumers to make purchases they might otherwise postpone. For many merchants, the additional sales generated by card acceptance far exceed the cost of processing payments.

This creates an interesting economic tension. Merchants frequently criticize interchange fees, yet many would likely see lower revenue if customers shifted back to cash-only purchasing behavior.

The hidden economics of interchange are that it is not simply a cost. It is also part of the infrastructure that encourages consumer spending and supports modern commerce.

The Future of Interchange

Interchange remains one of the most heavily debated areas in payments. Merchants argue that fees continue to rise and reduce profitability. Issuers argue that interchange funds fraud protection, innovation, rewards programs, and the security infrastructure consumers rely upon every day.

Regulators around the world continue to examine interchange structures, particularly for debit cards and dominant network participants. Ongoing legal and regulatory scrutiny in the United States suggests interchange economics will remain a major industry discussion for years to come.

What is unlikely to change is the central role interchange plays in modern commerce. Every time a customer taps a card, an intricate financial system springs into action. Funds move between institutions, risk is allocated, fraud protections are applied, and incentives are funded.

Most consumers never see it. Most merchants rarely think about it. Yet interchange remains one of the most important economic engines behind the global payments industry.