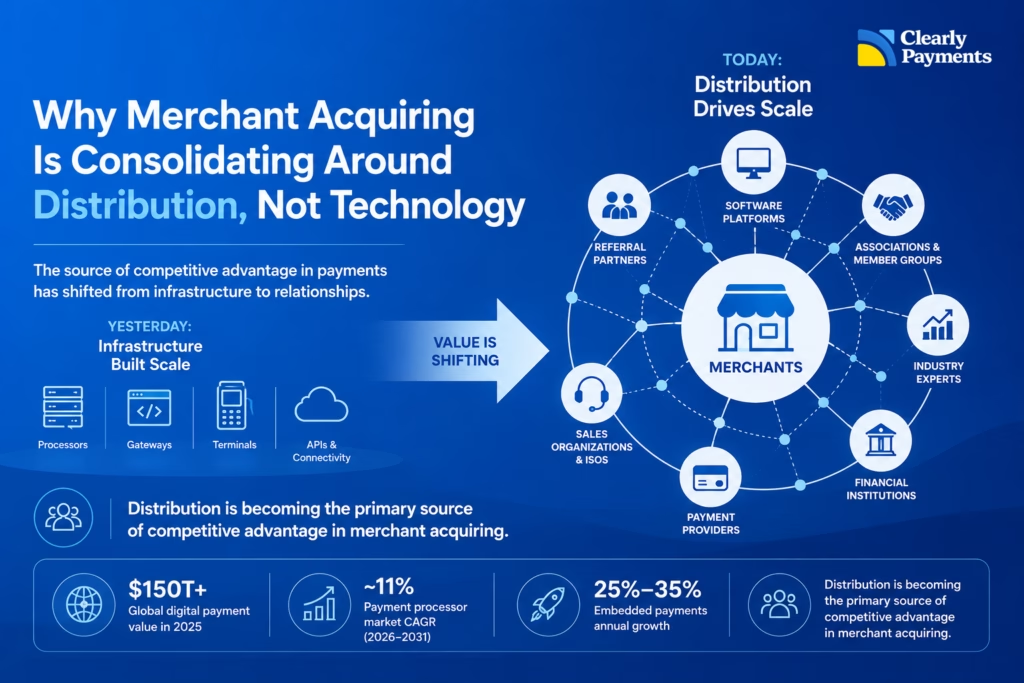

The payments industry has spent decades investing in technology. Processors built massive infrastructure platforms. Acquirers invested billions in connectivity, security, compliance, hardware certifications, and payment network integrations. The companies with the largest technology investments generally won because they could process transactions more efficiently, more reliably, and at greater scale than their competitors.

That model created some of the largest businesses in financial services. However, the economics of merchant acquiring have changed.

Payment technology remains essential, but it has become increasingly accessible and standardized. At the same time, merchant acquisition has become more expensive, customer ownership has become more valuable, and the businesses controlling distribution have gained strategic leverage.

As a result, a growing share of industry value is shifting away from infrastructure and toward distribution.

This trend helps explain the rapid growth of embedded payments, the continued value of independent sales organizations, the acquisition activity occurring across the payments ecosystem, and the increasing importance of merchant portfolios.

The future of merchant acquiring will still be powered by technology. But it will increasingly be controlled by those who own the customer relationship.

| Metric | Value |

|---|---|

| Global Digital Payment Value (2025) | $150T+ |

| Global Card Payment Volume (2025) | $50T+ |

| Payment Processor Market Size (2026) | $71B |

| Projected Market Size (2031) | $122B |

| Payment Processor CAGR | 11% |

Despite the size of the market, the fastest-growing areas are increasingly concentrated around businesses that own merchant relationships rather than payment infrastructure.

The payments industry continues to grow, but value is shifting

The global payments industry remains one of the largest and fastest-growing segments of financial services.

Worldwide digital payment transaction value is expected to exceed $150 trillion annually, while the payment processing market itself is projected to grow at roughly 10% to 12% per year over the next decade.

Yet some of the fastest-growing areas of the payment ecosystem are not infrastructure businesses. They are businesses that control merchant relationships.

| Segment | Estimated Annual Growth Rate |

|---|---|

| Payment Processing | 10%–12% |

| Embedded Finance | 16%–24% |

| Embedded Payments | 25%–35% |

| Vertical SaaS Payments | High Double Digits |

| Digital Commerce Payments | Double Digits |

The distinction matters.

Payment infrastructure continues to grow, but the highest valuations increasingly belong to businesses that own distribution. Software platforms, referral networks, integrated payments providers, merchant portfolios, and industry-specific ecosystems are all benefiting from this trend.

Investors are increasingly rewarding ownership of customer relationships rather than ownership of technology alone.

How merchant acquiring historically created value

To understand what is changing, it helps to understand how value was historically created.

Twenty years ago, payment technology represented a meaningful competitive advantage. Direct processor connections, network certifications, security infrastructure, underwriting systems, and risk management capabilities were expensive and difficult to build.

The industry’s structure reflected those realities.

| Source of Advantage | 2005 |

| Processing Infrastructure | Very High |

| Technology | High |

| Scale Economics | High |

| Distribution | Moderate |

A smaller competitor simply could not replicate the capabilities of a large processor.

Scale created lower costs. Lower costs funded additional investment. Additional investment strengthened the technology advantage.

This created a reinforcing cycle that helped large processors dominate the market. Today, many of those historical barriers have weakened.

Technology is becoming more accessible

Modern payment infrastructure is dramatically easier to access than it was a decade ago.

A new payment company can leverage established processors, gateways, embedded payments platforms, risk tools, and hardware ecosystems without building everything internally.

| Technology Layer | Common Providers |

| Processing Platforms | Fiserv, Global Payments, Worldpay |

| Payment Gateways | NMI, Cybersource, Authorize.net |

| Embedded Payments Infrastructure | Stripe, Finix, Payrix |

| POS Systems | Clover, PAX, Ingenico |

| Fraud & Risk Tools | Kount, Sift, Riskified |

For merchants, the practical result is that payment functionality is increasingly standardized. Most providers can offer online payments, recurring billing, digital wallets, reporting, fraud tools, and omnichannel acceptance.

Technology remains important, but it is no longer as scarce as it once was. When a competitive advantage becomes widely available, it becomes less valuable. That is exactly what is happening across large portions of the payments technology stack.

Distribution is becoming the new source of scale

As technology becomes more accessible, merchant relationships become more valuable.

The cost of acquiring a new merchant continues to rise. Competition has intensified. Merchants face constant outreach from processors, banks, software companies, and fintech providers. Winning trust and maintaining long-term relationships requires significant investment.

This is where distribution becomes powerful. In merchant acquiring, distribution generally falls into three categories:

| Distribution Type | Examples |

| Direct Distribution | ISOs, merchant sales organizations |

| Partner Distribution | Accountants, consultants, associations, referral partners |

| Embedded Distribution | Vertical SaaS and integrated payments providers |

While the models differ, they share one important characteristic.

They own access to merchants.

And increasingly, access to merchants is more difficult to replicate than payment technology itself.

Merchant relationships create extraordinary economic value

The value of distribution becomes clear when examining merchant economics. Consider a merchant processing $1 million annually.

| Metric | Value |

| Annual Processing Volume | $1,000,000 |

| Revenue Yield | 0.50% |

| Annual Revenue | $5,000 |

| Average Retention | 7 Years |

| Lifetime Revenue | $35,000 |

This example excludes growth in processing volume, equipment revenue, premium services, foreign exchange, lending products, payroll services, and other financial offerings.

In practice, the economic value can be significantly higher.

The important point is that merchant relationships often persist for many years. A gateway may change. A terminal may be replaced. A processor may merge with another company. Yet the merchant relationship itself frequently survives.

That durability creates recurring cash flow, which is why merchant portfolios continue to attract acquisition interest across the industry.

Follow the acquisitions

One of the clearest indicators of where value is moving is acquisition activity.

| Transaction | Approximate Value |

|---|---|

| Deluxe acquires Celero Commerce (2026) | $625M |

| Global Payments acquires EVO Payments | $4B+ |

| Shift4 acquires Revel Systems | $250M+ |

| Numerous ISO & portfolio acquisitions annually | Hundreds of Millions |

Over the past decade, acquirers have aggressively pursued businesses that control merchant relationships. These acquisitions include merchant portfolios, independent sales organizations, integrated payments businesses, referral networks, and vertical software companies.

Although these assets appear different on the surface, they share a common characteristic.

- They provide scalable access to merchants.

- A software company with 10,000 customers owns distribution.

- An ISO with 5,000 merchants owns distribution.

- An association with 20,000 members owns distribution.

- A referral network with thousands of introductions per year owns distribution.

Increasingly, buyers are paying for customer access rather than technology alone.

Embedded payments strengthen the thesis

Embedded payments are often cited as evidence that software companies will replace traditional merchant acquirers.

In reality, embedded payments reinforce the same fundamental trend. Software companies are valuable because they own distribution.

The software itself matters, but the true advantage comes from controlling the customer relationship. Once a platform becomes embedded in a merchant’s daily operations, payments become a natural extension of that relationship.

The same principle applies to successful ISOs and referral-driven payment companies. The delivery mechanism differs. The underlying economics do not.

In each case, the winner is the organization that owns merchant trust and controls access to the customer.

Artificial intelligence may accelerate the shift

Artificial intelligence is likely to make payment technology even easier to build and operate.

Customer support, onboarding, underwriting, fraud management, software development, and operational workflows are all becoming more automated. As these capabilities become more accessible, technology itself becomes less scarce.

Distribution does not.

Trusted relationships, industry expertise, referral networks, brand reputation, and merchant loyalty remain difficult to replicate. These advantages often take years to build and cannot be purchased off the shelf.

In many respects, AI may accelerate the migration of value toward distribution.

The easier technology becomes to create, the more valuable customer ownership becomes.

Merchant acquiring's competitive advantage has fundamentally changed

The payments industry will continue to innovate. New payment methods will emerge. Artificial intelligence will transform workflows. Embedded finance will expand into new industries.

Yet beneath these changes, a deeper shift is occurring. The source of competitive advantage in merchant acquiring is evolving.

Twenty years ago, the industry’s largest winners were the companies that owned the best infrastructure.

Tomorrow’s winners are increasingly likely to be the companies that own the strongest distribution.

That distribution may come through software platforms. It may come through referral networks. It may come through industry associations. It may come through independent sales organizations with deep merchant relationships and trusted brands.

The model matters less than the outcome. Technology enables transactions. Distribution owns customers.

And in a world where payment technology is becoming increasingly accessible, customer ownership is becoming the most valuable asset in merchant acquiring.