Spoiler: Processing rates are only one piece of the puzzle.

Many businesses choose a payment processor based on a simple comparison: 2.9% + 30¢ sounds easy, so it must be the best option. In reality, the true cost of accepting payments depends on much more than the advertised rate.

A processor that appears more expensive may save thousands of dollars each year. Likewise, a processor with a simple flat rate can become surprisingly costly as your business grows.

This guide explains the real differences between Stripe and a traditional merchant account, when each option makes sense, and how to calculate your actual payment processing costs.

At a Glance

| Feature | Stripe | Traditional Merchant Account |

|---|---|---|

| Setup | Minutes | Usually 1–3 business days |

| Pricing | Flat-rate | Interchange plus or custom pricing |

| Monthly Fees | Usually none | Sometimes |

| Contract | None | Varies by provider |

| Best For | Startups, developers, low volume | Growing businesses, established companies |

| Customer Support | Primarily online | Often dedicated support |

| Cost at Higher Volumes | Usually higher | Often significantly lower |

| Risk Reviews | Automated | Human underwriting available |

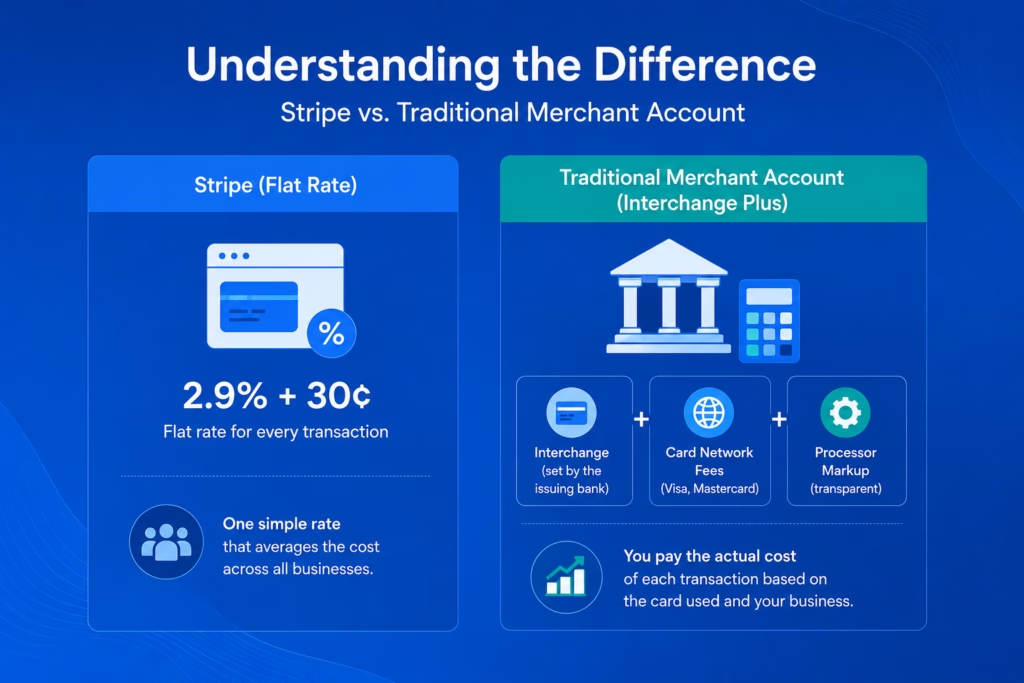

Understanding Stripe's Pricing

Stripe made online payments dramatically easier. Instead of negotiating rates or applying for a merchant account, businesses can begin accepting payments within minutes.

The tradeoff is pricing. A typical online transaction is charged:

2.9% + 30¢ per successful card transaction

While this is incredibly simple, it also means:

- Every business pays roughly the same rate

- Low-risk businesses subsidize higher-risk businesses

- Large businesses receive less benefit from their lower risk profile

For many startups, this simplicity is worth paying for.

For larger merchants, it often is not.

What Is a Traditional Merchant Account?

A merchant account is an individually underwritten payment account that connects your business directly to the card networks through a payment processor.

Rather than paying one flat rate, you generally pay:

- Card interchange fees

- Card network assessments

- A processor markup

This pricing model is commonly called Interchange Plus Pricing.

Instead of everyone paying the same rate, your pricing reflects the actual cost of each transaction. Businesses with stronger credit profiles, lower fraud rates, and lower chargeback rates usually benefit the most.

Why Flat-Rate Pricing Often Costs More

Flat-rate pricing must cover every possible transaction. That includes:

- Premium rewards cards

- Corporate cards

- High-risk merchants

- Higher fraud rates

- International cards

- Payment disputes

Because Stripe cannot predict which transactions you’ll receive, it averages the pricing across everyone. Think of it like insurance. Some customers cost very little. Others cost much more. Everyone pays approximately the same. Merchant accounts price businesses individually instead.

Example Cost Comparison

Imagine two online businesses processing the same amount.

Monthly Sales

- Revenue: $100,000

- Average transaction: $100

- Transactions: 1,000

Option 1: Stripe

| Cost | Amount |

| Percentage Fees | $2,900 |

| Per Transaction Fees | $300 |

| Total | $3,200 |

Option 2: Merchant Account

Example pricing:

- Average interchange: 1.55%

- Processor markup: 0.30%

- Monthly account fee: $20

| Cost | Amount |

| Processing | $1,850 |

| Monthly Fee | $20 |

| Total | $1,870 |

Estimated Savings

Approximately $1,330 every month. That’s nearly $16,000 per year.

Actual savings vary depending on card mix, transaction size, industry, and pricing structure, but for many established businesses the difference can be substantial.

It's Not Just About Rates

When businesses compare payment processors, they often focus on one number: the processing rate. In reality, the total cost of accepting payments depends on several factors that can have just as much impact as the advertised percentage.

A processor with a slightly higher monthly fee may actually cost less overall if it offers lower transaction costs, better pricing on premium cards, or tools that reduce chargebacks and fraud.

Here are some of the biggest factors that influence what you’ll actually pay.

Transaction Size Matters

Not every business processes payments the same way.

Imagine two companies that each process $10,000 in card sales.

A coffee shop might process 500 transactions averaging $20 each, while a furniture retailer processes only 10 transactions averaging $1,000.

Although total sales are identical, the coffee shop pays the fixed per-transaction fee hundreds of additional times. Over thousands of monthly transactions, those small fees can add up quickly.

Your Customers' Cards Affect Your Costs

Credit cards aren’t all priced the same.

Basic consumer cards generally cost less to process than premium rewards cards, corporate purchasing cards, or commercial cards. Traditional merchant accounts pass through these actual costs using interchange pricing, while flat-rate providers average everything into a single price.

For businesses whose customers primarily use lower-cost consumer cards, interchange-plus pricing often produces meaningful savings.

Chargebacks Can Be Expensive

Processing fees are only part of the picture.

Every chargeback can result in additional costs, including dispute fees, lost merchandise, administrative time, and higher fraud monitoring requirements.

Many traditional payment providers offer dedicated account support and fraud prevention tools that can help businesses reduce disputes before they become costly.

Payment Methods Continue to Expand

Customers increasingly expect more than just credit cards.

Digital wallets such as Apple Pay and Google Pay, Buy Now Pay Later services, and other alternative payment methods have become standard for many online businesses.

Stripe has built an excellent reputation for quickly supporting new payment technologies. Today, many traditional merchant account providers offer these same payment methods through modern gateways, although the available features can vary depending on the provider.

Looking Beyond Processing Fees

When evaluating payment providers, it’s important to consider the total cost of ownership rather than focusing solely on transaction rates.

Questions worth asking include:

- Are gateway fees included?

- What are the chargeback fees?

- Are PCI compliance costs extra?

- Are there monthly minimums?

- Is phone support available?

- How are refunds handled?

- What fraud prevention tools are included?

A provider with slightly higher monthly fees may still deliver lower overall costs if it reduces disputes, improves approval rates, or lowers processing expenses over time.

When Stripe Makes Sense

Stripe continues to be an excellent choice for many businesses.

It is particularly well suited for:

- Startups launching quickly

- SaaS companies

- Subscription businesses

- Developers who want powerful APIs

- Businesses processing relatively low monthly volumes

- Companies expanding internationally

For these businesses, the simplicity and flexibility of Stripe often outweigh the higher processing costs.

When a Traditional Merchant Account Makes Sense

Merchant accounts become increasingly attractive as businesses grow. They are often the better choice for:

- Established ecommerce businesses

- Healthcare providers

- Professional services firms

- Retail stores

- Manufacturers

- Home service companies

- Businesses processing more than $20,000 to $30,000 per month

As monthly processing volume increases, even small differences in pricing can translate into meaningful annual savings.

Can You Use Both?

Absolutely.

Many businesses use multiple payment solutions depending on how they operate.

For example, a company might use Stripe for recurring subscription billing while processing retail or higher-volume ecommerce transactions through a traditional merchant account.

This approach provides flexibility while allowing businesses to optimize costs where it matters most.

Frequently Asked Questions

Is Stripe more expensive than a merchant account?

Not necessarily. For businesses with lower transaction volumes, the cost difference may be relatively small. As processing volume increases, merchant accounts often become more cost-effective because pricing reflects the actual cost of each transaction rather than a flat average.

Why do larger businesses often switch to interchange-plus pricing?

Businesses with stable processing history and lower risk can often qualify for pricing that is significantly lower than flat-rate processing. As volume grows, those savings become increasingly meaningful.

Can I switch payment processors without disrupting my business?

In most cases, yes. Modern ecommerce platforms typically support multiple payment gateways, making it possible to migrate with minimal disruption when properly planned.

Does a merchant account still support Apple Pay and Google Pay?

Yes. Most modern merchant account providers support popular digital wallets and other payment methods through compatible payment gateways.