The use of cash and checks for payments has been steadily declining in recent years with more people choosing to use digital payment options instead. This trend is driven by a number of factors, including the convenience and security of digital payment methods, as well as changing consumer behavior and preferences.

Why cash is declining in popularity

One of the primary drivers of the decline in cash and check payments is the rise of digital payment options, such as credit and debit cards, mobile payments, and online payment platforms. These payment options offer a range of benefits over traditional payment methods, including convenience, speed, and security. Digital payments are also easier to track and manage, which can be especially useful for businesses and individuals who need to keep track of their finances.

In addition to the benefits of digital payment options, there are also some significant drawbacks to using cash and checks for payments. One of the biggest drawbacks is the risk of theft or loss. Cash can be easily stolen or misplaced, while checks can be lost in the mail or stolen from a mailbox. In contrast, digital payments are more secure and can be easily tracked and monitored, reducing the risk of fraud or theft.

Another factor contributing to the decline of cash and check payments is changing consumer behavior and preferences. As more people become comfortable with digital payment options, they are increasingly choosing to use them over cash and checks. This trend is particularly pronounced among younger generations, who are more likely to use mobile payment apps and other digital payment methods. The recent COVID pandemic has also made contactless payments more popular to help reduce transmission.

Despite the many benefits of digital payment options, there are still some challenges to overcome before cash and checks can be entirely replaced. Other than the cost of accepting credit card payments (interchange fees), one of the biggest challenges is ensuring that digital payment options are accessible to everyone, regardless of their income or technological literacy. In addition, some people may be reluctant to switch to digital payment options due to concerns about privacy and security.

There are a number of initiatives underway to address these challenges and promote the adoption of digital payment options. Governments and financial institutions are working to develop more inclusive and accessible digital payment systems, and many businesses are offering incentives for customers to use digital payment options.

How much is the use of cash declining?

The amount of cash used for payments varies depending on the country and region. However, according to recent studies, the use of cash for payments has been declining in many countries.

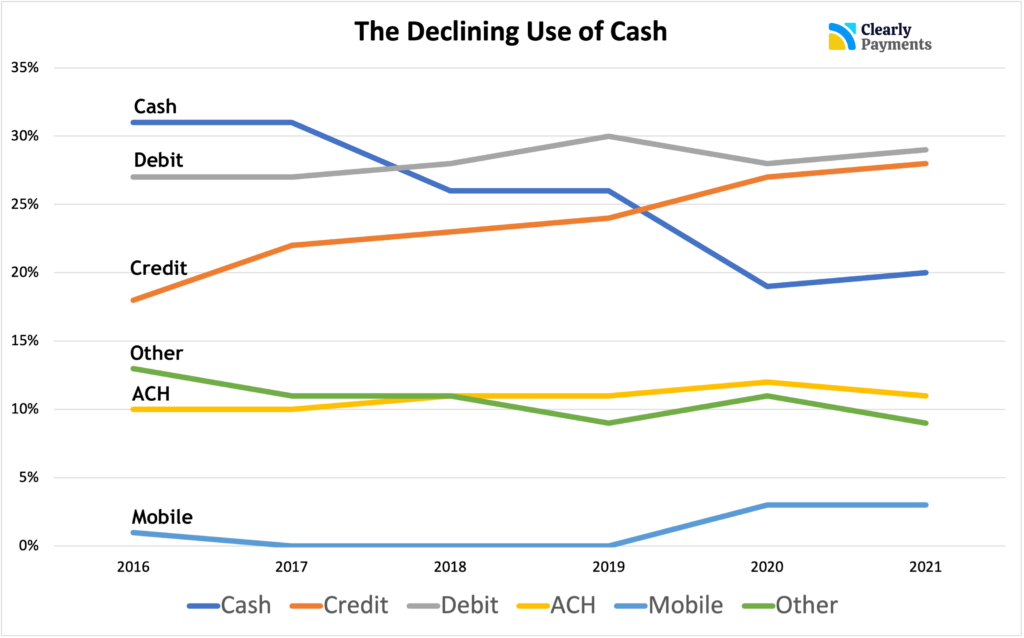

In the United States, the Federal Reserve Bank of San Francisco reported that cash usage has been declining steadily over the past decade. In 2019, cash was used for only 26% of all transactions, down from 30% in 2017. In contrast, card payments accounted for 50% of all transactions in 2019. Most predictions bring cash use into the single digit percentage points within the next seven years by 2030.

The data from the graph above is also replicated in the data chart below. It shows the percentage of transactions by payment type.

| Year | Cash | Credit | Debit | ACH | Mobile | Other |

|---|---|---|---|---|---|---|

2016 | 31% | 18% | 27% | 10% | 1% | 13% |

2017 | 31% | 22% | 27% | 10% | 0% | 11% |

2018 | 26% | 23% | 28% | 11% | 0% | 11% |

2019 | 26% | 24% | 30% | 11% | 0% | 9% |

2020 | 19% | 27% | 28% | 12% | 3% | 11% |

2021 | 20% | 28% | 29% | 11% | 3% | 9% |

Similarly, in the United Kingdom, a report from UK Finance showed that cash payments fell by 15% in 2019, while the use of contactless payments increased by 16%. The report also revealed that debit card payments surpassed cash payments for the first time in 2018.

In Sweden, cash usage has declined so rapidly that the country is on track to become the world’s first cashless society. According to the Swedish central bank, cash transactions now account for less than 13% of all payments, down from 40% in 2010.

The use of checks is also declining

The use of checks for payments has also been declining in recent years, although it still remains a common payment method in some countries.

In the United States, for example, the use of checks for payments has been declining for many years. According to a report from the Federal Reserve, check payments accounted for only 8.3% of all non-cash payments in 2018, down from 15.6% in 2012. The decline in check usage has been attributed to the rise of digital payment options, such as debit and credit cards, as well as online payment platforms.

Similarly, in the United Kingdom, the use of checks for payments has been declining steadily over the past few decades. According to a report from UK Finance, the number of checks processed in the UK fell by 40% between 2015 and 2018. The decline in check usage has been driven by the rise of digital payment options, as well as the increasing use of bank transfers and direct debit payments.

In other countries, the use of checks for payments is still more common. For example, in France, checks remain a popular payment method, accounting for around 16% of all payments in 2019, according to a report from the French Banking Federation. However, even in France, the use of checks has been declining in recent years, with the proportion of payments made by check falling from 25% in 2014.

The impact to the world of a cashless society

The decline of cash and check payments is having a significant impact on businesses, consumers, and the economy as a whole. Here are some of the primary implications of a world without cash.

Increased efficiency is one of the key benefits of digital payments. Digital payments can be processed quickly and easily, which can lead to increased efficiency in transactions. This can save time and resources for businesses and individuals. This will allow businesses to be more nimble so they can adapt to new opportunities. The data that comes with digital payments will also give businesses and consumers more information to make better decisions.

The use of digital payments can make it more difficult for criminals to engage in activities such as counterfeiting, money laundering, and tax evasion. Digital payments are much more traceable allowing authorities to follow a money trail. This will change the fraud environment, making it much more specialized.

Financial inclusion of different groups of people is a key implication, particularly in the short term. Digital payments can provide a way for people who do not have access to traditional banking services to participate in the economy. With digital payments, people can use mobile phones or other devices to make payments, even if they do not have a bank account. On another note, a cashless society could potentially exacerbate some existing inequities in society, as those who do not have access to digital payment methods, such as the elderly or those in rural areas, could be left behind.

Privacy concerns is another key topic of a cashless society. The rise of digital payments has raised concerns about privacy as digital transactions can be tracked and monitored more easily than cash transactions. This has led to calls for stronger data protection laws and increased transparency around how data is used. On these same lines, there is a vulnerability to cyber attacks, which could have significant economic and social consequences.