Interchange rates, also known as interchange fees, are the charges paid between banks for the acceptance of card-based transactions. These fees are a critical component of the payment processing ecosystem, affecting merchants, consumers, and financial institutions. In the European Union (EU), interchange rates have been a subject of significant regulation and debate, with a strong emphasis on promoting competition and protecting consumer interests.

This article covers the complexities of interchange rates in the EU, exploring their structure, regulation, and impact on the payment processing landscape.

A Background on the European Union (EU)

The European Union (EU) is a political and economic union of 27 member countries located primarily in Europe. Established by the Maastricht Treaty in 1993, the EU aims to promote peace, stability, and economic prosperity among its members through integrated policies and shared governance structures. The EU operates through a unique system of supranational institutions and intergovernmental negotiations, encompassing areas such as trade, law, environmental policy, and human rights.

The union has its own currency, the euro, used by 20 of its member states, collectively known as the Eurozone. The EU also maintains a single market, allowing for the free movement of goods, services, capital, and people among member countries, fostering economic cooperation and integration.

An Overview of Interchange Rates in EU

Interchange rates are typically paid by the merchant’s bank (the acquiring bank) to the cardholder’s bank (the issuing bank) whenever a card transaction is processed. These fees are designed to cover various costs, including fraud prevention, risk management, and transaction processing. The rates vary based on several factors, including the type of card (credit or debit), the nature of the transaction (domestic or cross-border), and the industry sector.

In the EU, interchange rates have traditionally been a contentious issue due to their perceived impact on both merchants and consumers. High interchange fees can lead to increased costs for merchants, which may be passed on to consumers in the form of higher prices. Conversely, these fees also support the infrastructure and services provided by issuing banks, including fraud protection and customer rewards programs.

Regulation and Fees of Interchange Rates in EU

The European Union has taken significant steps to regulate interchange fees to promote fairness and transparency in the payment processing market. One of the most notable regulatory measures is the Interchange Fee Regulation (IFR), which came into effect in December 2015. The IFR introduced caps on interchange fees for consumer debit and credit card transactions, setting a maximum of 0.2% of the transaction value for debit cards and 0.3% for credit cards.

In EU, they have set an interchange rate maximum of 0.2% for debit cards and 0.3% for credit cards.

The implementation of the IFR aimed to reduce the cost burden on merchants, particularly small and medium-sized enterprises (SMEs), and to encourage the use of card payments across the EU. The regulation also introduced measures to increase transparency, such as requiring payment service providers to disclose the interchange fees to merchants.

The impact of the IFR has been substantial. According to the European Commission, the regulation has led to an estimated annual reduction of €6 billion in interchange fee costs for merchants. This reduction has been particularly beneficial for SMEs, which often face higher relative costs for payment processing compared to larger businesses.

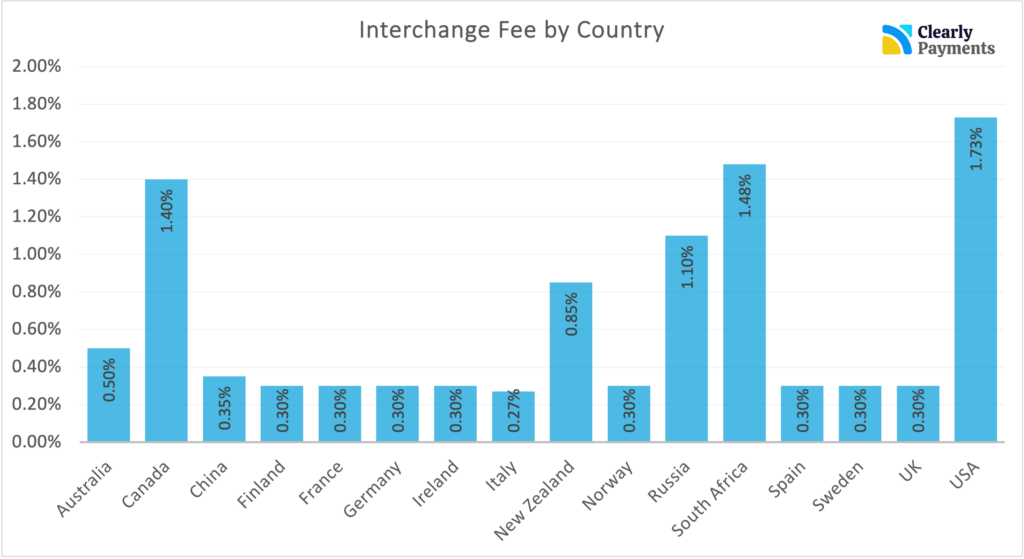

Overall, the regulation of payment processing in the EU has given it some of the lowest interchange rates in the world. Below is a chart on the interchange rates by country.

It’s important to keep in mind that interchange rates are just one of the fees that are paid for payment processing. Payment processors and payment platforms will also charge fees that increase the total cost that merchants pay. In general, these fees add an extra 0.30% (30 basis points) on top of interchange rates.

Impact on Payment Processing

The regulation of interchange rates has had a profound impact on the payment processing landscape in the EU. One of the key effects has been the increased competition among payment service providers. By capping interchange fees, the IFR has reduced the revenue that issuing banks can earn from card transactions, prompting banks and other payment service providers to seek alternative revenue streams and innovate in their service offerings.

This increased competition has benefited merchants by providing them with more choices and better terms for payment processing services. For example, many payment service providers have introduced lower-cost options for processing card transactions or have enhanced their offerings with value-added services such as data analytics and fraud prevention tools.

For consumers, the regulation of interchange rates has contributed to a more competitive and transparent market. While some feared that the reduction in interchange fees would lead to higher annual fees or reduced rewards on credit cards, studies have shown that the impact on consumers has been relatively limited.

Current Trends of Payments in EU

The payments landscape in the European Union (EU) is undergoing significant transformations, driven by technological advancements, changing consumer behaviors, and evolving regulatory frameworks. These trends are reshaping how payments are made, processed, and regulated, influencing both traditional financial institutions and emerging fintech companies. Here are some of the key current trends in payments across the EU:

Rise of Digital and Mobile Payments

Digital and mobile payments have seen rapid growth in the EU, accelerated by the COVID-19 pandemic. Consumers are increasingly favoring contactless payment methods for their convenience and security. According to a report by the European Central Bank (ECB), contactless payments accounted for more than 40% of in-person transactions in the EU in 2021, a significant increase from previous years.

Mobile payment solutions, such as Apple Pay, Google Pay, and local European digital wallets, have also gained traction. These platforms offer seamless integration with smartphones and other devices, enabling consumers to make payments with just a tap. The shift towards digital and mobile payments is supported by the widespread adoption of smartphones and the development of secure digital payment infrastructures.

Growth of E-commerce and Online Payments

The expansion of e-commerce has been a major driver of change in the payment landscape. The convenience of online shopping has led to a surge in online payment transactions. The EU’s e-commerce market reached a value of €717 billion in 2021, reflecting a growing preference for online shopping among consumers.

To support this trend, payment service providers have developed a range of solutions to facilitate secure and efficient online payments. These include payment gateways, secure checkout processes, and fraud prevention tools. The EU’s Payment Services Directive 2 (PSD2) has also played a role in enhancing security and fostering innovation in online payments by promoting the use of strong customer authentication (SCA). This has made fraud prevention like 3D Secure (3DS) mandatory in EU.

Emergence of Open Banking

Open banking is a transformative trend in the EU’s financial sector, driven by regulatory initiatives like PSD2. Open banking allows third-party providers to access consumers’ bank account information (with their consent) to offer tailored financial services. This has led to the emergence of new payment solutions and financial products, enhancing competition and innovation.

For example, fintech companies can leverage open banking to offer aggregated account information, personalized financial advice, and seamless payment services. The growing adoption of open banking is expected to further disrupt traditional banking models and create new opportunities for both consumers and businesses.

Increasing Importance of Real-Time Payments

Real-time payments are becoming increasingly important in the EU, providing immediate transfer of funds between bank accounts. This trend is supported by the development of infrastructures like the Single Euro Payments Area (SEPA) Instant Credit Transfer scheme, which allows euro transactions to be processed within seconds across participating countries.

Real-time payments offer several advantages, including enhanced liquidity management for businesses, reduced settlement risks, and improved consumer experiences. The EU is actively promoting the adoption of real-time payments as part of its broader strategy to enhance the efficiency and integration of the European payments market.

Focus on Security and Fraud Prevention

As the payment landscape becomes more digital and interconnected, security and fraud prevention are critical concerns. The EU has implemented stringent regulatory measures to protect consumers and businesses from payment fraud. PSD2’s strong customer authentication (SCA) requirements, for example, mandate two-factor authentication for many electronic payments, significantly enhancing transaction security.

In addition to regulatory measures, payment service providers and fintech companies are investing in advanced technologies such as artificial intelligence (AI) and machine learning to detect and prevent fraud. These technologies can analyze transaction patterns in real time, identifying suspicious activities and mitigating risks.