Choosing the right payment processor in Canada can materially impact your margins. Fees vary widely, contracts can be restrictive, and pricing models are often difficult to compare.

This guide breaks down the best payment processors in Canada, including a clear comparison table of fees, features, and real-world costs so you can make a confident decision.

Payment Processor Comparison Table (Canada)

Most providers advertise simple pricing, but the real costs depend on interchange rates, markup, monthly fees, and your specific mix of cards and transaction types. A flat percentage rarely tells the full story, especially as your business grows.

The table below simplifies the key differences across major providers in Canada so you can quickly compare pricing models, typical fees, and ideal use cases.

| Provider | Pricing Model | Typical Fees (CAD) | Monthly Fees | Best For | Notes |

|---|---|---|---|---|---|

| Stripe | Flat-rate | ~2.9% + $0.30 | None | Online businesses, SaaS | Easy setup, higher cost at scale |

| Square | Flat-rate | ~2.65% | None | Retail, small business | Simple, limited customization |

| Helcim | Flat-rate and Interchange+ | ~1.8%–2.6% | Low | Growing SMBs | Transparent pricing, strong value |

| Moneris | Tiered / Custom | High and Varies | Yes | Larger businesses | Long-term contracts common |

| Chase Payment Solutions | Interchange+ | High and Varies | Yes | Enterprise | Bank-backed, less flexible |

| Clearly Payments | Interchange+ | Lower blended rates | Low / None | SMB to mid-market | Optimized pricing + support |

A few important observations:

- Flat-rate providers are simple but often expensive as volume grows

- Interchange-plus pricing is usually cheaper but less understood

- Monthly fees can hide real cost differences

- Contract terms matter just as much as rates

What Are Payment Processing Fees in Canada?

Payment processing fees in Canada are not a single number. What you actually pay is made up of multiple layers, and understanding these is the key to reducing costs over time.

Most businesses focus only on the advertised rate, but the underlying structure matters far more.

1. Interchange Fees

These are set by card networks like Visa and Mastercard and are non-negotiable. They vary based on:

- Card type, credit vs debit

- Rewards level

- Whether the transaction is in-person or online

2. Processor Markup

This is the portion controlled by your provider. It can be structured in different ways:

- Flat-rate pricing

- Interchange-plus pricing

- Tiered pricing

3. Additional Fees

These are where many providers increase effective costs:

- Monthly account fees

- PCI compliance fees

- Chargeback fees

- Terminal and hardware costs

Over time, these additional costs often matter just as much as the base rate.

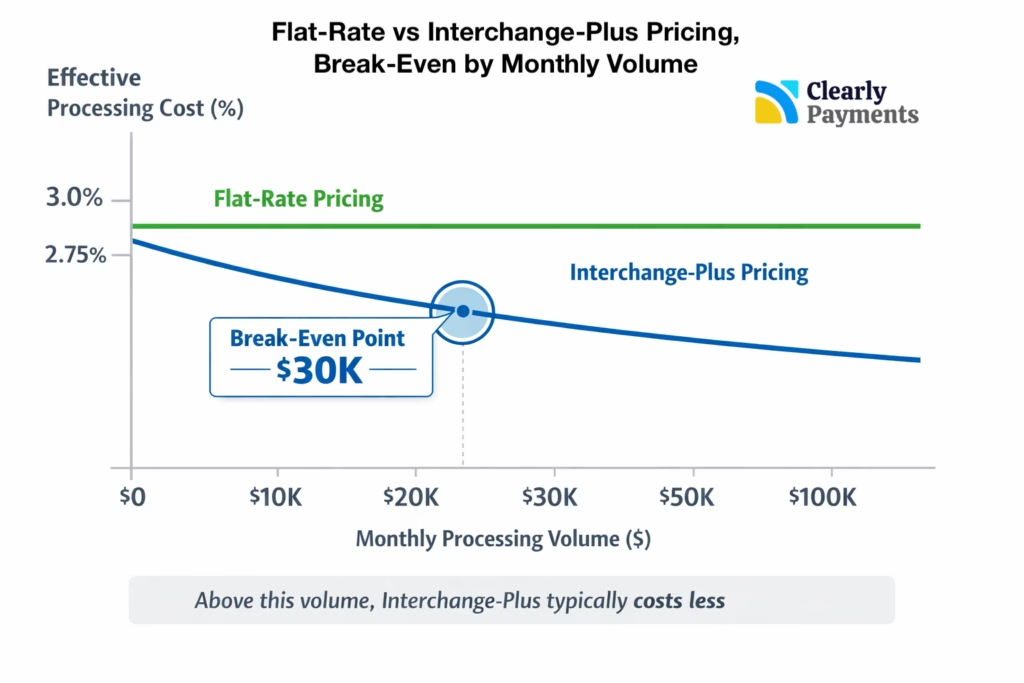

Flat-Rate vs Interchange-Plus Pricing

One of the most important decisions is choosing between flat-rate and interchange-plus pricing. While both are common in Canada, they behave very differently as your business scales.

Understanding this difference can save a meaningful percentage of your revenue.

Flat-Rate Pricing

Flat-rate providers like Stripe and Square offer a fixed percentage per transaction.

This works well for simplicity, but:

- You overpay on low-cost debit transactions

- There is little room for optimization

- Costs remain high as volume increases

Interchange-Plus Pricing

Providers like Clearly Payments and sometimes Helcim separate interchange from their markup, creating more transparency.

This typically results in:

- Lower effective rates

- Clear visibility into costs

- Better scalability as your business grows

For most businesses beyond early stage, with around $30k per month in sales, this model is more cost-efficient.

Best Payment Processors by Business Type

Not all processors are built for the same type of business. The right choice depends heavily on your size, sales channels, and how complex your payment needs are.

Matching your processor to your business stage is one of the easiest ways to avoid overpaying.

Small Businesses & Startups

Early-stage businesses often prioritize simplicity and speed over optimization.

Common choices:

- Square

- Stripe

These platforms are easy to set up, but typically come with higher fees.

Growing Businesses ($500K+ revenue)

As volume increases, even small differences in fees start to have a meaningful impact on margins.

Better options:

- Helcim

- Clearly Payments

These providers offer more competitive pricing and flexibility, making them better suited for scaling businesses.

Mid-Market & Enterprise

Larger businesses require more customization, better support, and stronger risk management capabilities.

Typical options include:

- Moneris

- Chase Payment Solutions

- Clearly Payments

At this level, pricing is usually negotiated and tailored to your specific needs.

Hidden Costs Most Businesses Miss

Many businesses believe they understand their processing fees, but hidden costs often erode margins over time. These are rarely highlighted upfront and can be difficult to detect without a detailed review.

Identifying these costs is often the fastest way to reduce total spend.

- Blended rate confusion: A single percentage can mask wide variation in actual costs

- Contract lock-ins: Long-term agreements may include early termination penalties

- Cross-border fees: Selling internationally can add 1%–2% or more per transaction

- Authorization and refund fees: These can accumulate quickly in e-commerce environments

How to Choose the Right Payment Processor

Choosing the right processor is not just about finding the lowest rate. It requires balancing cost, flexibility, and long-term fit with your business model.

A structured evaluation can prevent costly mistakes later.

- Volume: Higher volume businesses benefit more from interchange-plus pricing

- Sales channels: Online, in-person, and recurring payments have different requirements

- Average order value (AOV): Lower AOV businesses are more sensitive to fixed per-transaction fees

- Growth plans: Switching providers later can be disruptive, so plan ahead

Most businesses should compare at least two to three providers before making a decision.

Frequently Asked Questions

What is the cheapest payment processor in Canada?

Costs vary by business, but interchange-plus providers are generally the most cost-effective over time.

Is Stripe or Square better in Canada?

Stripe is typically better for online businesses, while Square is better suited for retail and in-person transactions.

Can I negotiate payment processing fees?

Yes. As your volume grows, most providers are willing to offer custom pricing.