In today’s global economy in 2024, the financial transactions has evolved into a dynamic ecosystem, where a multitude of players work together to facilitate fast and secure payment processing. From independent sales organizations (ISOs) and payment facilitators (PayFacs) to acquirers, card associations, and beyond, each entity plays a unique role in shaping the payment industry.

The payment processing ecosystem is vast and multifaceted, with a staggering array of statistics underscoring its significance. For instance, the global payment processing market is estimated to reach a monumental $587.78 billion by 2027, reflecting the indispensable role of these technical maestros in managing transaction authorization and settlement. Furthermore, global payment volume reached a staggering $31.7 trillion in 2023, emphasizing the sheer scale and impact of financial transactions on a global scale.

The proliferation of ewallet platforms and mobile payment systems over the past decade has also revolutionized the way consumers interact with financial services. As of 2023, there were over 4.5 billion mobile wallet users globally, highlighting the rapid adoption of these convenient and secure payment options.

Amidst this intricate dance of forces, competition reigns supreme, driving innovation and pushing the boundaries of convenience and accessibility. Whether it’s the fierce competition among acquirers for merchant accounts, the disruptive impact of emerging fintech startups, or the transformative potential of cryptocurrency and stablecoins, the competitive landscape is constantly evolving.

In this article, we give an overview of the complex ecosystem of payment processing, exploring the roles of various players, the dynamics of competition, and the ever-evolving landscape of financial transactions. From closed-loop payment networks and recurring billing solutions to cross-border payments and B2B payment platforms, we’ll examine the intricate interplay of forces shaping the future of commerce.

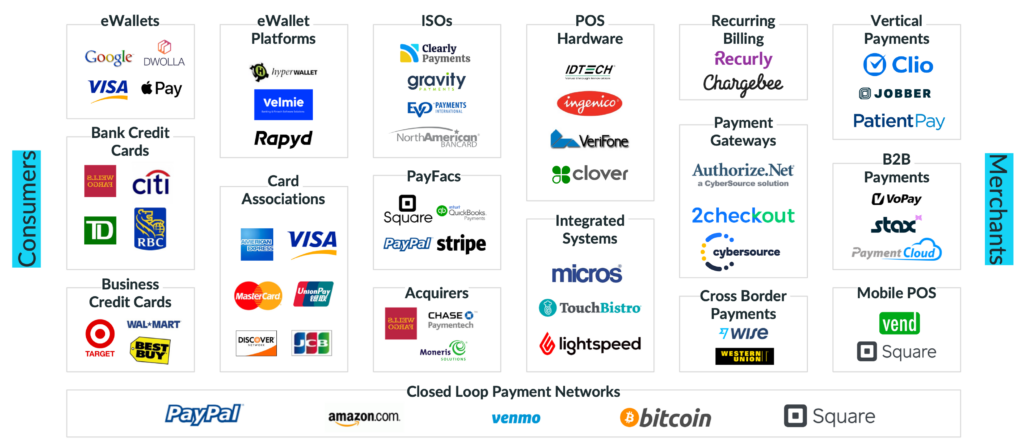

The Key Players in Payments

The cornerstone players in the payments industry lay down the essential infrastructure that enables seamless transactions. They establish standards, regulatory frameworks, and technology to ensure the safety and efficiency of payments in the industry along with getting payments in the hands of consumers and merchants. Typically, these are well-established companies with a wealth of experience and a strong foundation built over years of dedication to developing their business and fundamentals.

Card Associations (Credit Card Networks): Credit card networks like Visa and Mastercard govern the rules of credit and debit card transactions, facilitating the global movement of funds. In 2023, Visa alone facilitated a staggering $18.6 trillion in payment volume. However, they face challenges from emerging payment methods and evolving regulations.

Issuing Banks (Bank Credit Cards): Issuing banks are institutions that serve as the backbone for individual consumers, providing credit and debit cards. With over 7.2 billion cards in circulation in the US in 2022, they play a significant role. Yet, they grapple with issues such as fraud prevention and competition from innovative fintech startups.

Acquiring Banks: Acquiring banks act as the conduit for funds to reach merchants, these banks provide the infrastructure for card payments. The global acquiring market is expected to reach $3.7 trillion by 2027, but faces competition from alternative payment providers offering faster and cheaper solutions.

Payment Processors: These companies handle transaction authorization and settlement, ensuring smooth data exchange. The global payment processing market is estimated to reach $587.78 billion by 2027, but they face challenges in keeping up with technology and compliance.

Independent Sales Organizations (ISOs) and Payment Facilitators (PayFacs): These intermediaries connect merchants with acquirers and processors, generating significant revenue. These are not always large companies. They come in all shapes and sizes. However, ISOs are the primary channel of sales for all acquirers and payment processors. ISOs are registered with Visa and MasterCard and must navigate regulatory complexities and compete with direct access providers.

The Payment Ecosystem

The payment ecosystem has a large set of players beyond those mentioned above. It’s a dynamic and robust ecosystem that extends far beyond the surface. While the previous players provide the foundational systems and networks that facilitate payments, there exists a vast network of players who contribute to the development, distribution, and support of the payments market.

Below, we’ll explore the extensive network of software developers, distributors, and support providers that enrich and sustain this intricate ecosystem.

Supporting Players in the Payment Ecosystem

Payment Gateways: Payment gateways serve as the secure link between merchants’ systems and payment processors, they encrypt and transmit sensitive data. The global payment gateway market is projected to reach $49.7 billion by 2027, but must navigate security and regulatory challenges.

Mobile Payment Systems: Platforms like Apple Pay and Google Pay offer convenient payment options, with over 4.5 billion users globally as of 2023. Despite success, they face challenges in merchant acceptance and security concerns.

E-wallets: Digital wallets like PayPal facilitate online and in-store payments, with the global market expected to reach $26.41 trillion by 2027. However, they struggle with user acquisition and regulatory compliance.

Point-of-Sale (POS) Systems: POS systems manage sales transactions and accept various payment methods, playing a crucial role for merchants. The global POS systems market is projected to reach $152.39 billion by 2027, but must adapt to evolving needs.

Recurring Billing Systems: Recurring billing solutions automate recurring payments for subscriptions and memberships, essential for businesses like SaaS companies and gyms. The global recurring billing market is expected to reach $25.88 billion by 2027, highlighting their growing demand.

Buy Now, Pay Later (BNPL) Solutions: BNPL solutions offer consumers convenient short-term financing at checkout, BNPL providers like Klarna and Afterpay are rapidly gaining traction, with a transaction volume surpassing $165 billion in 2023. They disrupt traditional credit card usage and require merchants and regulators to adapt.

B2B Payment Solutions: Addressing the complexities of business-to-business (B2B) payments, these solutions often involve larger sums and specialized requirements. The global B2B payments market is projected to reach a staggering $25.7 trillion by 2027, signifying their significant role in business operations.

International Payment Solutions: Facilitating cross-border transactions, these services navigate currency exchange and regulatory hurdles. The global cross-border payments market is expected to reach $3.1 trillion by 2027, reflecting the increasing demand for seamless international transactions.

Vertical Industry Payment Solutions: Industry-specific software and hardware tailor payment options to the unique needs of sectors like healthcare or hospitality. This fragmented market holds immense potential for innovation and niche specialization.

Closed Loop Payment Networks

Closed loop payment networks refer to systems where a transaction is completed solely within a specific network or ecosystem, without involving external parties such as banks or credit card networks. These networks are “closed” because they only allow transactions among a defined group of participants, such as a particular merchant and its customers or a specific group of businesses and consumers.

In closed loop systems, transactions typically involve the use of proprietary payment methods, such as store-specific gift cards, loyalty or reward points, or prepaid cards issued by a single retailer or organization. These payment methods can only be used within the network or ecosystem for which they are designed. For example, a store gift card can only be used for purchases at that particular store or chain of stores.

There are also closed loop payment networks such as Paypal and Bitcoin. PayPal and Bitcoin facilitate transactions between users within its system but also across various platforms and networks.

Competitive Dynamics & Innovation in Payments

Competition fuels innovation and cost reduction within the ecosystem, with acquirers, processors, and new entrants vying for market share. In general payment companies want to either increase the dollar volume processed or increase the number of transactions.

Companies that want the dollar volume increased is likely due to their pricing model of charging a percentage of dollars processed (banks, credit card networks, processors, acquirers, etc). Companies that want a higher number of transactions, generally make most of their revenue with a transaction charge (payment gateways, wallets, etc).

Payment companies compete to win merchants through a variety of strategies aimed at offering competitive pricing, value-added services, and superior customer experience. The more merchants they have, the higher the dollar volume and number of transactions. Here are some ways they compete:

Pricing: Payment companies often compete by offering competitive pricing models, including interchange fees, processing fees, and monthly subscription fees. They may offer lower rates or discounts to attract merchants, especially high-volume businesses.

Value-added Services: Payment companies differentiate themselves by offering value-added services such as analytics, reporting tools, fraud detection and prevention, chargeback management, and customer support. These additional services can help merchants manage their businesses more effectively and efficiently.

Technology and Innovation: Companies compete by offering innovative payment solutions and technology that improve the merchant and customer experience. This includes features such as mobile payments, contactless payments, QR code payments, and integrations with POS systems and e-commerce platforms.

Customization and Flexibility: Payment companies may differentiate themselves by offering customizable solutions tailored to the specific needs of different industries or business sizes. They may also provide flexibility in contract terms, allowing merchants to scale their payment solutions as their business grows.

Customer Support: Excellent customer support can be a significant competitive advantage for payment companies. Providing responsive and helpful support to merchants can enhance their experience and loyalty to the payment provider.

Partnerships and Integrations: Payment companies may form partnerships with other service providers, such as accounting software, CRM systems, or e-commerce platforms, to offer integrated solutions that streamline operations for merchants.

Marketing and Branding: Effective marketing and branding strategies help payment companies stand out in a crowded market. This includes building a strong brand identity, creating targeted marketing campaigns, and participating in industry events and conferences.

Overall, payment companies compete to win merchants by offering a combination of competitive pricing, value-added services, innovative technology, customization, excellent customer support, strategic partnerships, and effective marketing and branding.

Potential Disruption in Payments

Open Banking: Open banking is a movement that will empower consumers to share financial data with third parties, this movement fosters innovation but disrupts traditional banks. It will allow the development of new software applications for consumers.

Cryptocurrency and Central Bank Digital Currencies (CBDCs): Governments exploring CBDCs could reshape the financial landscape, impacting existing players and creating new opportunities.

Buy Now, Pay Later (BNPL) Solutions: BNPL providers like Klarna and Afterpay offer short-term financing, potentially disrupting traditional credit card usage.

In conclusion, the commerce is a dynamic and evolving ecosystem, shaped by competition, innovation, and emerging trends. As new melodies emerge, traditional players must adapt, and new entrants must navigate regulatory complexities to orchestrate a harmonious financial future.