Choosing a payment processor in the U.S. is less about finding a single “best” option and more about matching the right pricing model and infrastructure to your business. The U.S. market is highly fragmented, with dozens of providers competing across different segments.

In 2026, most businesses are choosing between simplicity, cost optimization, and global capability. Understanding where you fall on that spectrum is what actually drives the decision. Typical U.S. pricing benchmarks:

- Online payments average around 2.9% + $0.30

- In-person payments typically range from ~2.4% to 2.7% + a fixed fee

Comparison: Top U.S. Payment Processors 2026

The U.S. payments landscape is dominated by a small group of platforms that each serve very different use cases. While they often look similar on the surface, their pricing models and strengths vary significantly depending on scale and complexity.

| Processor | Best For | Pricing Model | Typical Fees | Strength |

|---|---|---|---|---|

| Stripe | SaaS, marketplaces | Flat-rate | 2.9% + $0.30 | APIs, flexibility |

| Square | SMB retail | Flat-rate | 2.6% + $0.15 | Ease of use |

| PayPal | Online / trust | Flat-rate | ~2.99% + $0.49 | Brand recognition |

| Adyen | Enterprise | Interchange+ | Custom | Global scale |

| Checkout.com | High-growth | Interchange+ | Custom | Optimization |

| Helcim | Cost-conscious SMB | Interchange+ | Lower margins | Transparency |

| Clearly Payments | SMB to mid-market | Interchange+ | Custom / lower markup | Flexibility + support |

| Payment Depot | High volume | Membership + interchange | Lower per txn | Cost savings |

The 7 Best Payment Processors in the U.S.

The top processors in the U.S. are not interchangeable. Each one is optimized for a specific type of business, and choosing the wrong category often matters more than choosing the wrong provider.

1. Stripe — Best Overall for Online Businesses

Stripe has become the default infrastructure layer for modern internet businesses. Its strength lies in flexibility, developer tools, and the ability to support complex payment flows without heavy customization.

While it is extremely easy to start with, many businesses eventually outgrow Stripe due to pricing and risk controls.

- Built for developers and product teams

- Strong subscription and marketplace support

- Excellent documentation and APIs

Best for:

- SaaS companies

- Marketplaces

- Tech-enabled businesses

2. Square — Best for Small Businesses & Retail

Square is designed for simplicity and speed, making it one of the easiest ways for a business to start accepting payments. Its ecosystem combines software, hardware, and payments into a single platform.

Over time, however, its flat-rate pricing can become expensive compared to more flexible alternatives.

- Free POS software and hardware ecosystem

- Fast onboarding with minimal setup

- Strong in-person payment experience

Best for:

- Retail stores

- Restaurants

- Service businesses

3. PayPal — Best for Conversion & Trust

PayPal remains one of the most recognized payment brands globally, and that trust can translate directly into higher conversion rates at checkout. Many businesses use it alongside another processor rather than as a standalone solution.

Its pricing and account stability are the main trade-offs to consider.

- Widely recognized by consumers

- Strong international reach

- Easy to integrate alongside other processors

Best for:

- E-commerce brands

- Businesses with international customers

- Checkout optimization

4. Adyen — Best for Enterprise & Global Scale

Adyen is built for companies that operate at significant scale and require global payment infrastructure. Its platform combines acquiring, processing, and optimization into a single system.

The complexity of the platform means it is typically not suitable for smaller businesses.

- Interchange-plus pricing model

- Global acquiring and routing

- Advanced fraud and optimization tools

Best for:

- Enterprise companies

- Global brands

- Omnichannel retail

5. Clearly Payments — Best for Growing Businesses Seeking Lower Fees

Clearly Payments is positioned between simple flat-rate platforms and enterprise processors, offering a more flexible and cost-efficient alternative without adding unnecessary complexity.

For many businesses, it represents the point where optimizing fees and support starts to matter more than pure simplicity.

- Interchange-plus pricing with transparent markup

- More flexible underwriting and support

- Designed for long-term cost efficiency

Best for:

- Growing SMBs

Businesses moving off Stripe or Square - Merchants that want better pricing with enterprise level support

6. Helcim — Best for Transparent Pricing

Helcim focuses on simplicity and transparency, particularly around pricing. Unlike flat-rate providers, it uses an interchange-plus model with clearly defined margins.

This makes it one of the more cost-effective options for businesses that want visibility into their fees.

- Interchange-plus pricing

- No long-term contracts

- Automatic volume discounts

Best for:

- Professional services

- SMBs optimizing costs

- Businesses seeking transparency

7. Checkout.com — Best for High-Growth Companies

Checkout.com sits between Stripe and enterprise providers, offering more optimization and control without the full complexity of platforms like Adyen. It is designed for businesses that are scaling quickly and need better performance.

Its value increases significantly as transaction volume grows.

- Strong approval rate optimization

- Global payment coverage

- Flexible infrastructure

Best for:

- Scaling e-commerce companies

- International businesses

- High transaction volume

8. Payment Depot — Best for High-Volume Savings

Payment Depot uses a membership-style pricing model that separates processing fees from provider margins. This approach can significantly reduce costs for businesses processing higher volumes.

However, it only becomes advantageous once a certain scale is reached.

- Monthly membership pricing

- Lower per-transaction costs

- Predictable fee structure

Best for:

- Businesses processing $500K+ annually

- Companies focused on margin optimization

How U.S. Businesses Actually Choose

Most comparison guides focus on features and surface-level pricing, but real-world decisions are driven by volume, risk, and operational needs. Businesses typically start with simplicity and move toward optimization as they grow.

The transition point is where many businesses either improve margins or continue overpaying.

Volume determines pricing leverage

As processing volume increases, the cost difference between flat-rate and interchange-plus pricing becomes meaningful. This is often the trigger to switch providers.

Risk affects approval and stability

Processors prioritize risk management, which impacts approval rates and account stability. In many cases, this matters more than pricing.

Technical resources shape the decision

Companies with engineering teams often choose flexible platforms like Stripe, while others prioritize ease of use and support.

Approval rates impact revenue

Even small improvements in approval rates can have a measurable impact on revenue.

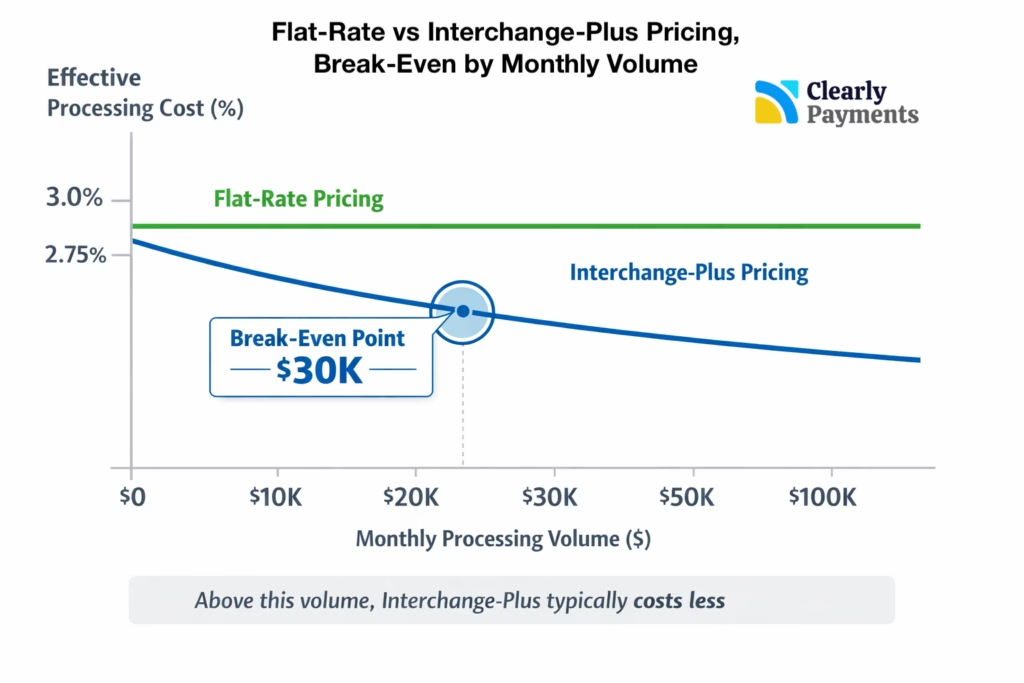

Flat Rate vs Interchange-Plus (Simple Breakdown)

The pricing model you choose will directly impact your long-term costs. Understanding the trade-offs is critical before making a decision.

| Model | Pros | Cons | Who It’s For |

|---|---|---|---|

| Flat-rate | Simple, predictable | Expensive at scale | SMBs, startups |

| Interchange-plus | Lower cost, transparent | More complex | Growing businesses |

| Enterprise | Optimized, flexible | Requires scale | Large companies |

Most businesses begin with flat-rate pricing and only later optimize. The key is recognizing when that shift should happen.

- Flat-rate is easy but expensive over time

- Interchange-plus reduces costs at scale

- Flexibility and support become more important as businesses grow