The Durbin Amendment has reshaped the U.S. financial system since it began in 2010. Named after its chief advocate, Senator Richard Durbin, this legislative moved was designed to fix the increasing interchange fees charged by banks for debit card transactions.

By limiting debit card fees, the amendment tried to make a more fair financial ecosystem, promoting competition and benefiting small businesses and everyday debit card users.

Why the Durbin Amendment Exists

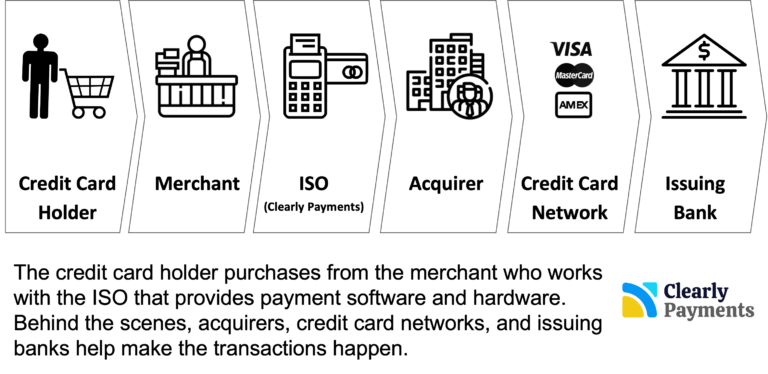

Debit card transactions involve a set of players in the payments value chain: the issuing bank (that provides the debit card to the consumer), the acquiring bank (that processes the transaction for the merchant), the payment network (like Visa or Mastercard), and merchant services provider (i.e. ISO or aggregator).

Interchange fees are a largest portion of the transaction amount paid by the acquiring bank to the issuing bank for authorizing and settling the transaction. They are also the payment processing fees that are paid by the merchant at the end of the day.

Prior to the Durbin Amendment, interchange fees were set by payment networks and were not subject to direct regulation. Prior to the Durbin Amendment, merchants would typically see debit card fees as 2% plus $0.40 per transaction.

Concerns arose that these fees were excessively high, placing a burden on merchants and potentially leading to higher prices for consumers. The Durbin Amendment aimed to address this concern by empowering the Federal Reserve to regulate interchange fees for debit card transactions.

Key Provisions of the Durbin Amendment

The Durbin Amendment gives the Federal Reserve the authority to set “reasonable” maximums on interchange fees for debit card transactions. The Durbin Amendment focuses on regulating debit card interchange fees and fostering competition within the payment processing industry. Here are its key provisions:

Interchange Fee Cap: The amendment limits the fees that banks issuing debit cards can charge retailers for processing debit card transactions. This puts the maximum fee at a set amount, currently at 0.05% and $0.21 per transaction.

Network Routing: It mandates that debit card transactions be routed over at least two unaffiliated payment networks. This promotes competition among networks like Visa and Mastercard, ensuring merchants have access to multiple options.

Restrictions on Anti-Competitive Practices: The Durbin Amendment prohibits exclusive arrangements between debit card networks and issuing banks. This prevents networks from locking merchants into using only their services.

Merchant Freedoms: The amendment allows retailers to offer incentives to customers for using alternative payment methods like cash, debit cards from other networks, or loyalty programs. It also permits merchants to refuse accepting debit cards for small transactions where fees might outweigh the benefit.

Fees Before and After the Durbin Amendment

The Federal Reserve established a maximum limit of $0.021 per transaction plus an additional 0.05% of the transaction amount. An additional $0.01 increase could be authorized for fraud prevention initiatives.

The difference between 0.05% and $0.21 per transaction after the Durbin Amendment is much lower that the average fee of 2% and $0.40 per transaction before the Durbin Amendment. This has brought significant savings for merchants. This move has made debit cards much cheaper for merchants to use than credit cards.

The Impact of the Durbin Amendment

The intended result of the Durbin Amendment was to lower costs for merchants who process debit card transactions. These savings could then be passed on to consumers in the form of lower prices. However, the effectiveness of the Amendment in achieving this goal is a matter of debate. Merchants are definitely paying less, however it does not mean that consumers are paying less.

Proponents argue that the Amendment has successfully reduced interchange fees, leading to potential cost savings for merchants. Opponents, however, contend that merchants have not consistently passed these savings on to consumers.

There are also some people that argue that the Amendment has reduced innovation in the debit card market, as issuing banks have less revenue to invest in new technologies and security measures.

Controversies, Debates, and Problems Over the Durbin Amendment Today

This legislation has stirred significant controversy and debate across various sectors. Key issues include its impact on small banks and credit unions, the actual benefits passed on to consumers, adjustments in bank fees, the distribution of benefits between merchants and consumers, and ongoing legal challenges.

Impact on Small Banks and Credit Unions: Although the Durbin Amendment caps fees only for large banks (those with over $10 billion in assets), there has been concern about indirect impacts on smaller financial institutions. These smaller banks are not subject to the fee cap, but they may feel competitive pressures to lower their fees in line with the larger banks, potentially reducing their revenue.

Effect on Consumer Prices: One of the primary goals of the Durbin Amendment was to lower costs for consumers by reducing merchant fees that could be passed on as savings. However, there’s been significant debate over whether merchants actually pass these savings onto consumers.

Bank Fee Increases: In response to the revenue loss from capped interchange fees, many large banks have increased other charges, such as monthly account fees and minimum balance requirements, or reduced benefits like free checking.

Legal and Regulatory Challenges: The Durbin Amendment has faced various legal challenges and calls for reconsideration or repeal. Banks and payment networks have lobbied against the amendment, arguing that it imposes arbitrary constraints on their business models and interferes with market dynamics.