MOTO payments refer to credit card transactions where customers provide their payment details via mail, telephone, or other non-face-to-face methods to complete a purchase. Credit card information is typically passed in a voice conversation and the merchant enters the information into a payment terminal.

MOTO payments have been around for decades, originally serving as an alternative payment method for customers who couldn’t physically visit a store or merchant location. The rise of eCommerce and the advent of remote shopping have given MOTO payments a new life to a certain extent. However businesses, particularly those operating online, can process transactions from customers located anywhere in the world with online payments, rather than over the phone with MOTO payments.

What is MOTO in payments?

MOTO stands for Mail Order/Telephone Order. It is a type of payment processing that allows merchants to accept credit card payments for goods or services over the phone or through the mail. To be clear, MOTO generally means speaking over the phone where your customer tells you their credit card number or using physical mail. It is not a credit card payment on a mobile app, email, or computer.

MOTO payment processing is commonly used by businesses that do not have a physical store, such as online businesses or mail-order companies.

With MOTO payments, the merchant manually enters the customer’s credit card information into a virtual terminal or a payment gateway. A MOTO transaction is a card-not-present (CNP) transaction. The transaction is processed just like any other credit card transaction, with the credit card network authorizing the payment and the merchant receiving the funds in their account.

MOTO payments can be a convenient option for customers who do not have access to a physical store or who prefer not to make purchases online. They can also be a good option for merchants who want to expand their customer base beyond their local area or who want to offer additional payment options to their customers.

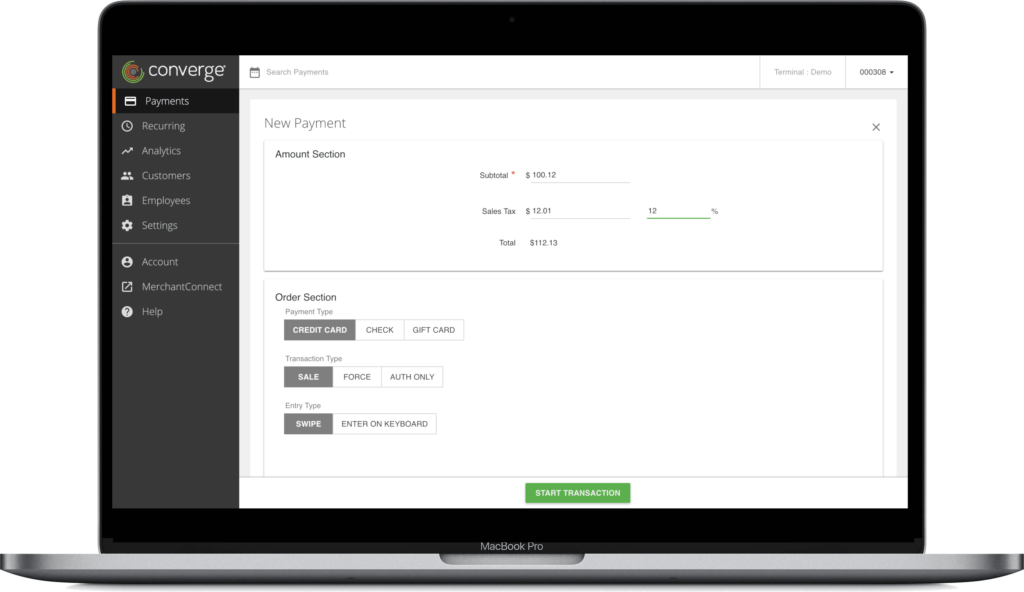

How a merchant processes a MOTO transaction?

In a MOTO (Mail Order/Telephone Order) credit card transaction, the merchant enters the customer’s credit card information into a virtual terminal or a credit card machine to process it.

Virtual Terminal: A virtual terminal is a web-based application provided by a payment processor or payment gateway. It allows merchants to manually enter credit card information and process transactions without the need for a physical card reader. Merchants access the virtual terminal through a web browser on their computer or mobile device. A merchant can conduct a credit card transaction by just entering credit card details into a virtual terminal.

Credit Card Machine (Payment Terminal): A credit card machine also known as a payment terminal or point-of-sale (POS), is a device used by businesses to process payments made by customers using credit or debit cards. These machines are typically found in brick-and-mortar retail locations, restaurants, and various other businesses where face-to-face transactions occur. The primary function of a credit card machine is to securely capture and transmit payment information to complete a purchase. However, a merchant can conduct a credit card transaction by just entering credit card details without the card being present.

It is very simple and fast to take a credit card payment by manually entering the credit card number, expiry date, and security code (CVV).

The advantage of MOTO transactions

Among the various payment methods available to businesses and consumers, MOTO payments (Mail Order/Telephone Order) provides numerous benefits that cater to the needs of commerce.

Global Reach: Moto payments allow businesses to serve customers across borders, transcending geographical limitations and expanding their customer base.

Convenience: Customers appreciate the convenience of making purchases without leaving their homes or offices. This flexibility attracts more consumers to choose MOTO payments over traditional methods.

Subscription-Based Services: Moto payments are popular among businesses offering subscription-based services, as they can also enable recurring payments as well as single transactions.

Risk with MOTO transactions

While Moto payments offer various advantages, they also come with unique security challenges. As payments occur without physical card verification, businesses must implement robust security measures to protect customer data. Encryption, tokenization, and multi-factor authentication are some of the essential tools in safeguarding sensitive information during Moto transactions.

MOTO payments can also be more risky than other types of payment processing. Because the merchant manually enters the customer’s credit card information, there is a higher risk of human error, such as entering the wrong credit card number or expiration date. Additionally, because the transaction is not conducted in person, there is a higher risk of fraud or chargebacks.

To minimize the risk of fraud and chargebacks, merchants who use MOTO payments should take steps to verify the customer’s identity and ensure that the transaction is legitimate. This may include asking for additional verification, such as the customer’s billing address or the CVV code on the back of their credit card.

With the continued growth of eCommerce and the increasing demand for remote shopping, Moto payments could have further expansion. Technological advancements, such as voice-activated payments and artificial intelligence-driven security features, will likely enhance the convenience and security of Moto transactions.