In the world of online and card-not-present (CNP) transactions, security is of utmost importance. To combat fraudulent activities and provide an additional layer of protection, credit cards are equipped with a Card Verification Value (CVV) which also has other names, but is generally called the credit card security code.

In this article, we will explore how the security code works, its purpose, and its role in enhancing the security of payment transactions.

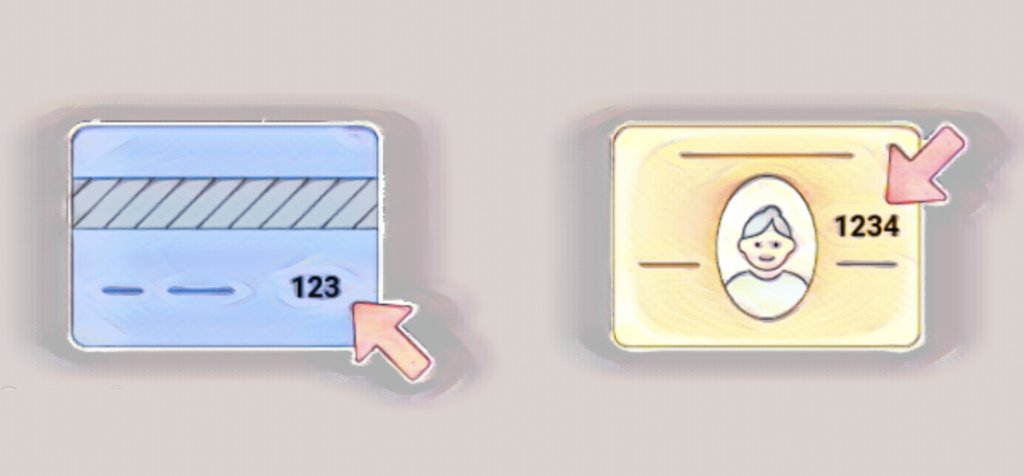

What is a CVV?

The Credit Card CVV (Card Verification Value) is a three or four digit security code that is typically printed on the back or front of a credit card. It is an additional security feature implemented by card issuers to help verify the authenticity of the card during online or card-not-present transactions.

The CVV is not embossed or raised on the card’s surface like the card number and expiration date. Instead, it is usually printed flat and consists of three digits for Visa, Mastercard, and Discover cards, while American Express cards have a four-digit CVV. The location of the CVV may vary depending on the card network and issuer.

During an online transaction, the CVV is requested by the merchant to confirm that the cardholder has physical possession of the card. It acts as a verification code that helps reduce the risk of fraud by ensuring that the person making the purchase possesses the card details, including the CVV.

As the CVV is not encoded on the magnetic stripe or chip of the card, it provides an additional layer of security and helps protect against unauthorized or fraudulent transactions. It is generally recommended to keep the CVV confidential and not share it with others to maintain the security of the card and minimize the risk of misuse.

Location and formats of the security code

The Card Verification Value (CVV) on credit cards is also known by various other names depending on the credit card network:

Card Verification Code (CVC): CVC is the term used by Mastercard for the three-digit security code printed on the back of the card, typically in the signature panel.

Card Security Code (CSC): CSC is the term used by Discover and American Express for the four-digit code printed on the front of the card, usually above the card number.

Card Identification Number (CID): CID is the term used by American Express for the four-digit code printed on the front of the card, typically above the card number. It is also sometimes referred to as the “Unique Card Code” (UCC).

Card Verification Value 2 (CVV2): CVV2 is the term used by Visa for the three-digit code printed on the back of the card, usually in the signature panel.

It’s important to note that while the names may vary, the purpose of these codes remains the same which is to provide an additional layer of security and help verify the authenticity of the card during card-not-present transactions.

Purpose and function of CVV

The primary purpose of the CVV is to enhance the security of payment transactions, particularly in card-not-present scenarios. Here’s how it works:

Verification of Card Ownership: When making an online or over-the-phone purchase, the merchant typically requests the CVV along with the card number and expiration date. By providing the correct CVV, the cardholder demonstrates that they possess the physical card, adding an extra layer of authentication.

Protection against Unauthorized Transactions: The CVV helps reduce the risk of fraudulent activities, as it is not typically stored in merchant databases or captured during transaction processing. Even if unauthorized individuals gain access to other card details, they would still need the CVV to complete a transaction successfully.

Compliance with Payment Card Industry Standards: The Payment Card Industry Data Security Standard (PCI DSS) mandates that merchants and payment processors must not store CVV data after authorization. This further protects cardholder information and minimizes the risk of data breaches.

Difficulties in Counterfeit Card Creation: CVV adds an additional layer of complexity for fraudsters attempting to create counterfeit cards. Without the CVV, counterfeit cards become significantly less valuable for unauthorized transactions.

Limitations of CVV

The Card Verification Value (CVV) is an important security feature, but it does have limitations that should be taken into consideration. Firstly, it is primarily designed for card-not-present (CNP) transactions, such as online purchases or phone orders, and it is not intended to provide the same level of verification for face-to-face transactions where the physical card is present. This means that the CVV alone cannot guarantee the authenticity of the cardholder in such scenarios.

Secondly, while the CVV helps verify that the person making the transaction has possession of the card, it does not provide full protection against the use of stolen cards. If someone gains unauthorized access to both the card details and the CVV, they can still use them for fraudulent transactions. Therefore, it is crucial to promptly report a lost or stolen card to the card issuer and take appropriate actions to protect oneself.

Furthermore, the CVV is vulnerable to card skimming techniques. Skimming involves unauthorized individuals capturing card data, including the CVV, through devices or techniques, which can be used for fraudulent purposes. Although advancements in card security, such as chip-enabled cards, have mitigated this risk to some extent, it is still important to remain vigilant and protect card information.

It is also worth noting that the CVV does not verify the cardholder’s identity. It solely confirms that the person making the transaction has the physical card and its associated CVV. This means that even if the CVV is provided correctly, it does not guarantee the legitimacy of the cardholder.

Additionally, in certain situations, such as recurring billing or card-on-file transactions, the CVV may not be required or validated. While this enhances convenience for customers, it also poses a risk if unauthorized individuals gain access to stored card details, as they can potentially use them for fraudulent purposes without needing the CVV.

Lastly, the effectiveness of the CVV relies on the security measures implemented by merchants and payment processors during online transactions. Weak security protocols, data breaches, or vulnerabilities in online systems can potentially expose CVV data, compromising its effectiveness as a security measure.