Many business owners don’t realize that payment processing is a little more complex than it seems. From hidden fees to chargeback risks, there’s a lot that payment providers don’t always disclose upfront.

In this article, we’ll break down the essential facts, statistics, and insider knowledge you need to navigate the payment processing landscape effectively.

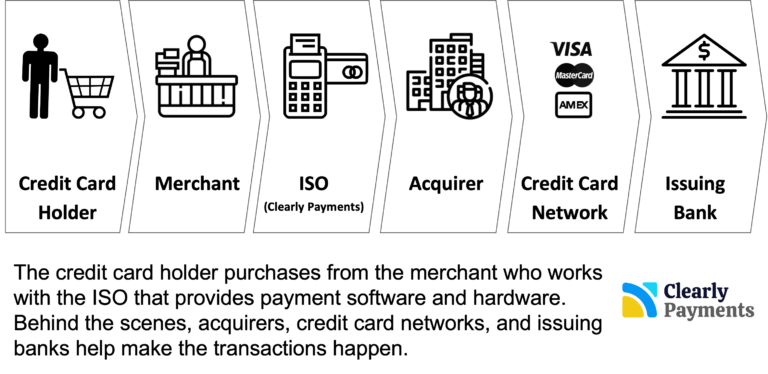

The Basics of Payment Processing

Payment processing involves multiple players, including:

The Merchant – The business accepting the payment.

The Customer – The person making the payment.

The Payment Processor – The company that facilitates transactions.

The Acquiring Bank – The acquiring bank receives funds on behalf of the merchant.

The Issuing Bank – The customer’s bank, called the issuing bank, which authorizes or declines transactions.

Card Networks – Companies like Visa, Mastercard, and American Express (credit card networks) that set processing rules and fees.

The Costs You Don’t See

One of the biggest surprises for small businesses is the actual cost of accepting credit and debit cards. Here’s a breakdown of what you might be paying:

Interchange Fees – These are set by card networks and typically range from 1.5% to 3.5% per transaction. Here’s an overview of interchange fees.

Processor Markup – Payment processors add their own fees, which can be 0.2% to 1% above interchange fees.

Monthly Fees – Some processors charge a flat monthly rate, often between $10 and $50.

Chargeback Fees – If a customer disputes a transaction, you could pay between $20 and $100 per chargeback.

PCI Compliance Fees – PCI compliance are for ensuring your business follows security standards can cost around $100 to $300 per year.

The Truth About “Flat-Rate” Processing

Many small businesses are drawn to flat-rate pricing because it seems simple, with rates like 2.9% + 30¢ per transaction (common with providers like Square and PayPal). However, while this model is predictable, it’s often more expensive than interchange-plus pricing, which separates actual interchange fees from processor markup. Businesses processing over $10,000 per month may find interchange plus pricing options significantly cheaper.

Chargebacks: A Hidden Risk

A chargeback occurs when a customer disputes a transaction, and the money is refunded to them, often at the merchant’s expense. Here are some chargeback facts:

Small businesses lose an average of $3.75 for every $1 disputed due to fees, lost inventory, and operational costs.

Fraud-related chargebacks account for 70% of all disputes.

The chargeback rate should stay below 1%—going above this can lead to fines or even account termination.

It takes 60-90 days to resolve a chargeback, meaning cash flow can be disrupted.

Cash Discounting and Surcharging

To offset processing costs, some businesses use cash discounting or surcharging:

Cash Discounting – Offering a small discount (usually 3-4%) for customers who pay with cash instead of a card.

Surcharging – Adding a surcharging processing fee (often 3%) to credit card transactions to pass costs onto customers.

While legal in most U.S. states, these strategies come with compliance requirements, and surcharging is prohibited for debit cards.

Mobile Payments and Contactless Transactions

Consumer payment preferences are shifting:

72% of consumers now prefer digital payments over cash.

Contactless payments grew by 150% between 2020 and 2023.

Mobile wallet usage (Apple Pay, Google Pay) has increased by 80% since 2019.

Offering mobile and contactless payment options can improve customer experience and increase sales.

Cross-Border and International Transactions

For small businesses looking to expand internationally with cross-border payments, payment processing comes with additional challenges and costs:

Currency Conversion Fees – Banks and payment processors typically charge 1-3% to convert foreign currencies.

Higher Interchange Fees – International card transactions often have 0.5% to 1% higher fees compared to domestic transactions.

Settlement Delays – International payments can take 2-5 days to process due to multiple banking systems involved.

Regulatory Compliance – Businesses must comply with rules like GDPR (Europe), PSD2 (EU), and AML/KYC laws in various countries.

Fraud Risks – Cross-border transactions have twice the fraud risk compared to domestic payments, leading to stricter verification measures.

To manage these challenges, businesses can work with global payment processors that offer localized payment methods, multi-currency accounts, and advanced fraud prevention tools.

How to Reduce Payment Processing Costs

Negotiate Your Rates – If you process over $50,000 per year, you can ask for lower fees.

Use an Interchange-Plus Pricing Model – It’s usually cheaper than flat-rate pricing.

Avoid High-Risk Transactions – Large or unusual transactions can trigger fraud reviews, increasing costs.

Implement Fraud Prevention Tools – Address Verification Systems (AVS) and 3D Secure can reduce fraud risk.

Review Statements Regularly – Hidden fees can creep in over time; always check your monthly statement.