Interchange rates are a cost for credit card transactions for merchants. Interchange is the revenue for credit card companies and issuing banks.

Canada and the USA have a big overlap in purchasing habits and trends in payments. The two countries also have some big differences on how payment processing fees work across debit cards and credit cards.

This article aims to provide an overview and comparison of the interchange rates in the United States and Canada.

An Overview of Interchange Rates

Interchange rates are often referred to as swipe fees or credit card fees. They are the fees charged by the card card issuing bank to the merchant for transactions made with a credit card. Interchange rates also exist for debit cards in the USA, but not in Canada. This is one of the key differences between Canada and the USA payment fees.

Interchange rates are set by credit card networks such as Visa, Mastercard, and AMEX which are generally revised every year. The rates merchants pay change based on factors like the type of card used, the merchant’s industry (MCC code), and the transaction method (e.g., in-person, online, and keyed).

Interchange rates impact the cost of accepting card payments for merchants and influence the rewards and benefits offered to credit card holders. When merchants understand how interchange fees work, there are things they can do to decrease credit card processing fees. This is one reason why it’s important for merchants to do some research.

USA Interchange Rates

In the United States, interchange rates are known for their complexity. There are literally hundreds of rates. Rates can differ based on the card type (credit, debit, rewards, corporate, etc.), the size of the transaction, and the merchant’s industry.

A standard retail transaction might have an interchange rate of around 1.51% to 2.52% of the transaction amount for credit cards, while debit card transactions typically have lower rates, often below 1%.

The U.S. has seen regulatory changes, such as the Durbin Amendment, which capped interchange fees for certain debit card transactions. This regulation has led to a two branches in debit card rates with lower fees for large banks (those with assets over $10 billion) and relatively higher fees for smaller banks.

Here is a full overview of USA interchange rates.

Canada Interchange Rates

In comparison to the U.S., Canada’s interchange rates are generally perceived as more streamlined, though they still vary by card type and transaction method. Credit card rates in Canada tend to range from about 1.25% to 2.4% of the transaction amount.

Debit card rates, on the other hand, are significantly lower, often less only a fixed transaction fee of about $0.08. It’s important to note that debit cards and Visa Debit cards are priced very differently. Visa Debit do incur fees similar to debit fees in USA.

In recent years, there has been pressure from the Canadian government and merchant associations to lower interchange rates to reduce the cost burden on merchants. As a result, major card networks have voluntarily agreed to reduce average rates, leading to a slight downward trend in overall interchange fees.

Here is a full overview of Canada interchange rates.

Interchange Rate Comparison and Implications

In general, the interchange rates and the total amount that USA merchants pay is slightly higher in than merchants in Canada. The below table highlights the key interchange pricing differences between Canada and the USA for Visa credit cards.

This table compares the most basic Visa credit card with a top Visa rewards credit card along with each in card present (i.e. in-store transaction) and card not present (i.e. online transaction).

This is just as an example because there are many interchange rates in Canada and even more in the USA. Overall, the USA has roughly 15% higher interchange fees than Canada which you can also see in our report on interchange fees by country.

| Transaction Type | Canada Interchange Rates | USA Interchange Rates |

|---|---|---|

| Card Present Swipe/Chip with Basic Credit Card | 1.25% | 1.510 % + $0.10 |

| Card Not Present Online/Keyed with Basic Credit Card | 1.40% | 1.900 % + $0.10 |

| Card Present Swipe/Chip with Rewards Credit Card | 2.08% | 2.100 % + $0.10 |

| Card Not Present Swipe/Chip with Rewards Credit Card | 2.40% | 2.520 % + $0.10 |

When comparing interchange rates between the USA and Canada, there are several key differences:

- Complexity: U.S. interchange rates are generally more complex, with a wider range of rates based on many more factors. Canadian rates are more streamlined with fewer categories and less variability.

- Regulation: The U.S. has seen more regulation of interchange rates, particularly for debit cards through the Durbin Amendment. Canada has relied more on voluntary agreements with card networks to manage rates. Canada also has a payments code of conduct.

- Rate Levels: While rates vary widely, U.S. credit card interchange rates are often higher on average than those in Canada. However, the gap has been narrowing over the years.

- Debit Card Rates: Debit card rates are significantly lower in Canada than in the USA.

The USA has roughly 15% higher interchange rates than its neighbour Canada.

The differences in interchange rates between the USA and Canada have some implications for businesses and consumers:

- Merchant Costs: Canadian merchants face lower card acceptance costs, especially for debit card transactions, compared to their U.S. counterparts.

- Pricing and Profitability: Differences in interchange rates affect the pricing strategies and profitability of businesses operating in both countries. Payment processors have higher margins in the USA than in Canada.

- Consumer Rewards: Higher interchange rates in the U.S. support more generous credit card rewards programs compared to Canada.

The Breakdown of Average Fees Merchants Pay

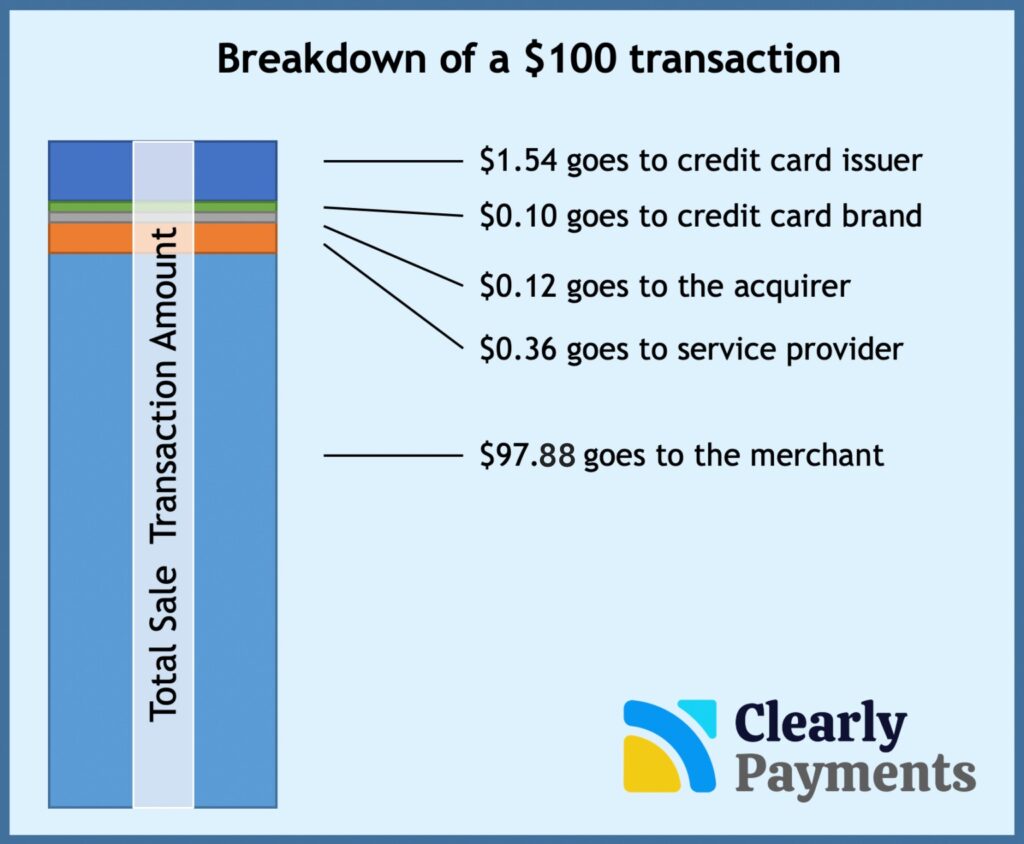

It is important to keep in mind that the interchange fee is not the total fees that merchants pay for payment processing. The interchange fee makes up the biggest part of the processing fees that merchants pay, often exceeding 80%.

The average total fees merchants pay for a credit card transaction is approximately 2.20% in Canada and 2.45% in the USA.

There are other fees such as the network fees, processor markup, and depending on the processor and setup, there might be additional charges for things like terminal rentals, payment gateway fees (for online transactions), and PCI compliance fees (related to data security). All these fees are on top of the interchange fees.

The above chart is a simplified example to show the general breakdown of a transaction where the merchant fee was 2.12%. It shows where the fees go and the amount the merchant keeps for a $100 transaction