Merchants not only “overpay” because they chose the wrong provider. They overpay because their pricing model is opaque, their card mix drifts toward premium and commercial cards, and small “leaks” like downgrades, cross border fees, and unnecessary add-ons quietly stack up.

In 2026, lowering your effective rate is still very doable, but it takes a research-style approach, measure your baseline, isolate the drivers, then pull the highest impact levers.

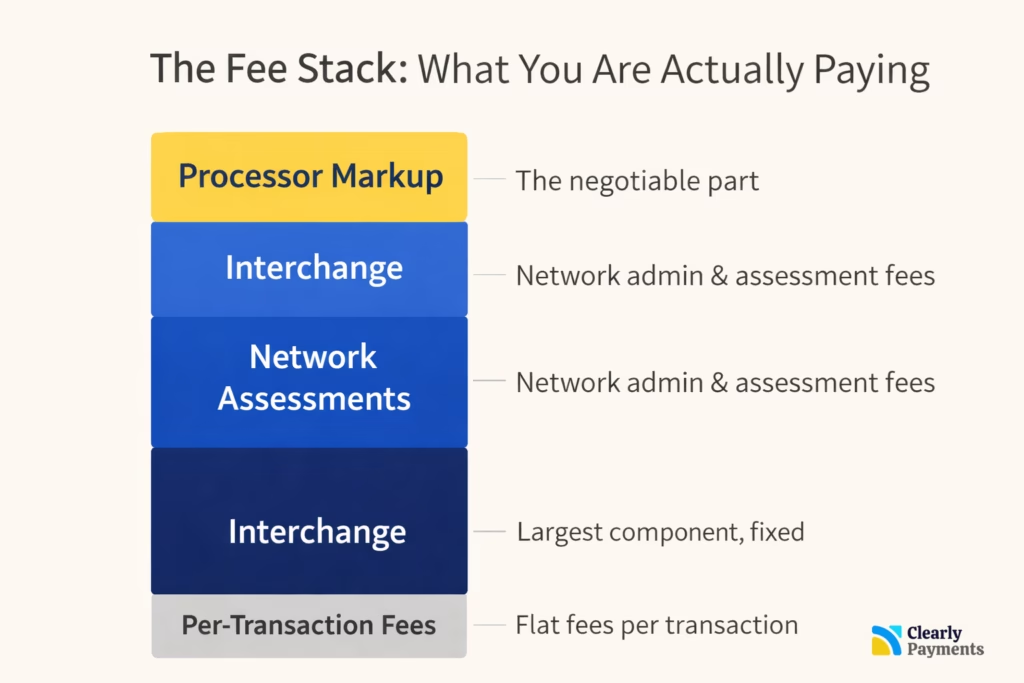

The Fee Stack and What you are Actually Paying

Your all-in card cost, often shown as an “effective rate,” is usually:

Interchange + network assessments + processor markup + per-transaction fees + extras divided by your total credit card sales

Interchange is the biggest line item, and it varies by card tier, merchant category, and how the transaction is processed. Visa, for example, publishes interchange tables and updates, including changes effective April 18, 2026 for consumer credit categories.

Processor markup is the part you can negotiate most directly, and competitive interchange-plus pricing commonly shows up as a % markup plus a per-transaction fee.

Step 1: Calculate your Baseline (the Only Number that Matters)

Before you change anything, compute these for the last 90 days:

Total card volume

Total processing fees (everything, including monthly, PCI, gateway, terminal, statement, network fees)

Effective rate = total fees ÷ total volume

Then break fees into buckets:

- Interchange (often shown in interchange-plus statements)

- Assessments and network fees

- Processor markup

- Per item fees

- Monthly and “misc” fees (PCI, gateway, terminal, statement)

If you cannot clearly see these buckets, that is a sign you are on a pricing model that makes optimization harder. We can help review your statements if you want clarity.

Step 2: Pull the Biggest Levers First

Lever 1: Move to interchange-plus, then negotiate markup

If you are on bundled, tiered, or flat rate pricing, your true margin is hidden. Interchange-plus makes costs auditable and negotiable.

A practical benchmark to sanity-check your offer is whether your markup is in a competitive range for your size and risk profile, and whether per-transaction fees are reasonable. (In USA and Canada, competitive ranges commonly land in the band of a modest % markup plus a few cents per transaction, depending on volume and risk.)

What to ask for in writing:

- Markup as interchange + X% + $Y (percentage market and transaction fee)

- A full list of monthly fees, gateway fees, PCI fees, terminal fees

- Confirmation of any “non-qualified” or downgrade pricing triggers

Quick win: many merchants can shave 0.10% to 0.40% off effective rate by tightening markup and eliminating junk fees, even before operational changes.

Lever 2: Fix downgrades, they are silent profit killers

Downgrades happen when a transaction fails to meet the network’s best-qualification criteria, and it slips into a higher-cost category.

Common downgrade causes:

- Card not present transactions missing required data

- Incorrect MCC or setup

- Poor settlement timing, batch delays

- Recurring payments not flagged properly

- Incomplete AVS, CVV, or ecommerce indicators where applicable

What to do

- Pull a downgrade report from your processor

- Identify top downgrade reasons, fix settings in gateway and POS

- Confirm your MCC is correct for your business

Even small downgrade rates can add meaningful basis points over a year.

Lever 3: Optimize your card mix, because premium cards cost more

Rewards and premium cards usually carry higher interchange than basic cards. Credit Card Networks publish interchange schedules that make this visible, and they update categories over time.

Merchant-friendly ways to shift mix:

- Encourage debit for smaller tickets where customers are indifferent

- Offer a small discount for lower-cost methods where allowed

- Use signage and checkout UX prompts that make debit or low-cost options easy

General payment Code of Conduct is designed to support transparency and merchant choice, including pricing flexibility to encourage lower-cost payment options.

Lever 4: Use surcharging or discounts carefully, and legally

In Canada and USA, merchants can surcharge credit card transactions with strict rules, including disclosure, limits, and generally a maximum surcharge cap of 2.4%, with some regional restrictions.

Practical guidance

- If you surcharge, do it cleanly, posted at point of sale and on receipts, and never stack it with a “service fee” on the same transaction.

- If you do not want surcharge friction, discounts can be a softer approach, and the Code of Conduct supports discounting by payment method and network.

Lever 5: Route more volume through Interac Debit where it fits

For many merchants, debit is the cost-control workhorse, especially in person.

Interac’s own reporting highlights continued growth in debit usage, including increased SMB transaction counts in parts of 2025.

Where debit routing helps most

- Low-margin retail

- Convenience, quick service

- Any business with lots of sub-$50 tickets

This is not about pushing customers, it is about giving a clear, easy option when customers do not care.

Step 3: Cut the “Extras” that Inflate your Effective Rate

Lever 6: Remove or reduce monthly fees that do not earn their keep

Common offenders:

- PCI “non-compliance” fees that persist even after compliance

- Gateway fees you do not need

- Statement fees, “program” fees, “regulatory” fees without explanation

- Terminal insurance, terminal leases

Rule: if you cannot explain a fee in one sentence, challenge it.

Lever 7: Audit cross border and currency costs

If you sell online, accept foreign cards, or settle in multiple currencies, cross border related network fees can add up.

For example, acquirers and processors may pass through network “non-domestic settlement” style fees that can change over time.

What to do

- Measure % of volume that is foreign

- Confirm how FX is handled, and whether you are paying multiple layers (FX margin + network fee + processor uplift)

Lever 8: Reduce chargebacks and fraud, not just for loss, but for pricing

Higher fraud and chargeback rates can push you into higher risk pricing and more reserves.

Operational fixes:

- Strong AVS and CVV where applicable

- 3DS for ecommerce where it makes sense

- Clear descriptors and customer support paths to prevent “friendly fraud”

Even if you “win” disputes, high ratios can still raise future costs.

Lever 9: Improve authorization and batching habits

Authorization declines and late batching cost money indirectly, lost sales, more manual retries, and sometimes qualification issues.

Best practices:

- Settle daily, consistently

- Ensure terminal and gateway settings match your business type

- Keep software and terminals updated

Lever 10: Match pricing to your real profile

The best deal for a low-risk, stable merchant is different than for a high-risk vertical or a fast-growing ecommerce brand.

Bring these to negotiations:

- 12 months volume

- Average ticket

- Refund rate

- Chargeback ratio

- Top card types and channels (in-store vs online)

The more “boring and predictable” your stats look, the more leverage you have.

A Simple Savings Model you can Plug your Numbers into

Let’s say you do $1,000,000 per year in card volume.

- Cutting effective rate by 0.20% saves $2,000 per year

- Cutting by 0.50% saves $5,000 per year

- Cutting by 1.00% saves $10,000 per year

These improvements usually come from a combination of markup, fee cleanup, and reducing downgrades.

Merchant Checklist for 2026

If you only do 6 things, do these:

- Calculate effective rate for the last 90 days

- Demand a fee breakdown by bucket

- Switch to interchange-plus if you are not on it

- Remove junk monthly fees, leases, and duplicate add-ons

- Fix downgrades via gateway and settlement settings

- Decide on a steering strategy, debit prompts, discounts, or compliant surcharging