If your business accepts credit cards, chargebacks are a part of doing business. Chargebacks can impact your business’s revenue, reputation, and customer relationships. With rising fraud and online shopping, efficiently managing a chargeback team can be a big differentiator for your business.

This guide provides an overall approach to managing a chargeback team, covering everything from key roles and responsibilities to leveraging technology, monitoring performance, and incorporating data-driven strategies.

What are Chargebacks in Payment Processing?

A chargeback is a reversal of a credit card transaction initiated by the cardholder’s bank, usually as a result of a dispute by the customer over the purchase. It acts as a consumer protection tool, allowing customers to reclaim funds for unauthorized transactions, fraud, or dissatisfaction with goods or services.

Here are some other resources on chargebacks:

The Role of a Chargeback Team in a Business

A chargeback occurs when a customer disputes a charge with their card issuer, leading to the reversal of a payment. While chargebacks were originally introduced as a consumer protection tool, they are frequently used in cases of fraud or simply as a means of securing a refund quickly (friendly fraud). A well-organized chargeback team minimizes these risks and protects the merchant’s bottom line.

Key Activities of a Chargeback Team

- Reviewing Dispute Notices: Receiving and thoroughly investigating dispute notices from credit card issuers is the first task. This involves understanding the dispute reason codes and the customer’s claims.

- Evidence Collection: Gathering supporting evidence such as transaction receipts, delivery confirmations, and customer communication logs.

- Filing Representments: The chargeback team must then submit compelling evidence to the acquiring bank or card network to counter the chargeback and recover the revenue.

- Analyzing Patterns: Chargeback data should be reviewed regularly to spot patterns in disputes, enabling the team to implement proactive measures to reduce the number of future chargebacks.

- Preventing Fraud: Developing strategies to minimize chargebacks, whether caused by fraud or by disputes, ensures a healthier merchant profile and reduces financial loss.

Building and Structuring a Chargeback Team

To manage chargebacks effectively, you’ll want to create a team that includes poeple skilled in finance, customer service, and fraud prevention. The following roles are the most common in a chargeback team:

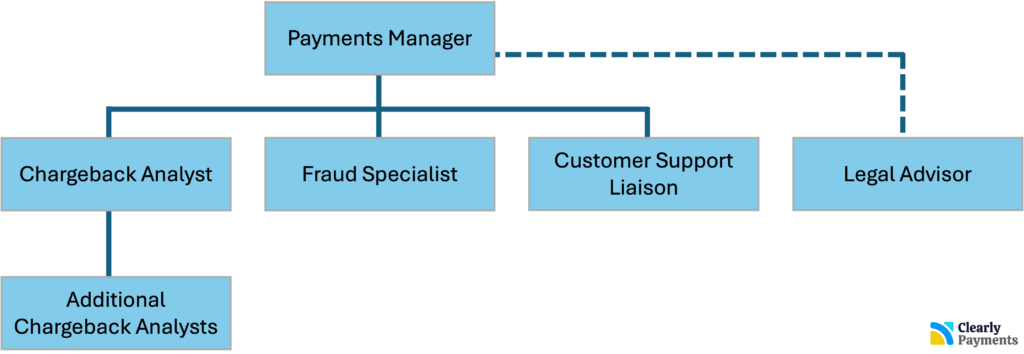

- Payments Manager: This role can be the head of finance or a dedicated manager that is responsible for the team dealing with chargebacks. This role also communicates with payment processors and banks.

- Chargeback Analyst: Responsible for reviewing disputes, gathering evidence, and analyzing chargeback data to identify trends. A background in finance, accounting, or data analysis is a plus. There could be many chargeback analysts, depending on the number of chargeback your company gets, which would then require a team of analysts. Each chargeback analyst should be able to handle 200 to 400 chargebacks per month.

- Fraud Specialist: Focuses on investigating potential fraud, preventing fraudulent transactions, and working closely with the analyst to minimize the risk of chargebacks related to fraud.

- Customer Support Liaison: Ensures smooth communication with customers, addresses complaints before they escalate into disputes, and promotes customer satisfaction to minimize chargeback instances.

- Legal Advisor: In complex chargeback cases, having legal expertise can be essential, particularly in disputes involving large amounts or multiple fraud claims.

Chargeback Team Organizational Structure

How the Chargeback Team Works Together

Managing a chargeback team requires coordination between specialized roles to minimize disputes and protect revenue. Each team member has a specific function, but their effectiveness comes from how well they collaborate.

1. Chargeback Analyst: The Investigator

The chargeback analyst reviews dispute notices and collects evidence to fight chargebacks. They work with various departments to gather data:

- Customer Support: Provides communication records that help clarify the customer’s complaint.

- Sales and Operations: Supplies transaction and shipping details needed for representment.

- Fraud Specialist: Shares insights on potential fraud-related disputes.

2. Fraud Specialist: The Guardian

The fraud specialist identifies fraudulent transactions to reduce chargebacks.

- Collaboration with the Analyst: Works together to investigate whether a chargeback is linked to fraud or friendly fraud.

- Prevention: Provides recommendations for improving fraud detection tools like 3D Secure and Address Verification Service (AVS).

3. Customer Support Liaison: The Bridge

Customer service is often the first point of contact for resolving customer issues before they escalate into chargebacks.

- Works with the Analyst: Provides communication history with the customer for evidence.

- Prevention Role: Resolves disputes early, reducing the likelihood of a chargeback being filed.

4. Legal Advisor: The Protector

In complex or high-value disputes, the legal advisor ensures compliance with regulations and assists in developing a robust defense during the representment process.

- Collaboration with the Analyst: Advises on handling complex chargeback cases and navigating card network rules.

5. Technology & Automation: The Enabler

Automated chargeback management platforms streamline processes, helping teams manage cases, track deadlines, and quickly file representments.

Best Practices for Managing a Chargeback Team

Managing a chargeback team requires a combination of good planning, efficient processes, and continuous improvement. Implementing best practices helps your team operate effectively, reducing chargebacks and safeguarding revenue. Here are key strategies to help your chargeback team succeed.

1. Leverage Technology to Streamline Processes

Automating your chargeback management process greatly increases efficiency. Today’s merchants can utilize chargeback management software platforms that streamline data collection, track deadlines, and organize communication between departments.

Some chargeback management tools use machine learning and AI to detect patterns in fraudulent transactions, identify friendly fraud, and even automate the submission of evidence to issuing banks.

Key Statistic: According to a study by Juniper Research, the cost of online payment fraud is expected to exceed $48 billion by 2023. Leveraging automation and AI can reduce the manual workload on your chargeback team by up to 30%.

2. Establish Clear Communication Channels

Successful chargeback management relies heavily on internal and external communication. Internally, it’s important that your customer service, accounting, and chargeback teams work together seamlessly. Customers are more likely to file chargebacks if their issues aren’t addressed quickly through customer service.

Externally, communication with acquiring banks, payment processors, and customers should be handled with precision and professionalism. Responding to chargeback notifications promptly, gathering required documents on time, and submitting evidence without delay is essential.

Key Statistic: Around 86% of chargebacks are the result of customer service issues that could have been avoided with better communication.

3. Set Measurable KPIs and Benchmarks

Establishing key performance indicators (KPIs) helps measure the effectiveness of your chargeback team. Some KPIs to track include:

- Win/Loss Ratio: The percentage of chargebacks that were successfully fought and won.

- Chargeback-to-Sales Ratio: This measures the number of chargebacks compared to total sales, helping you understand whether your chargeback rate is within acceptable limits. The credit card networks typically require this ratio to be under 1%.

- Response Time: The speed at which your team responds to chargebacks is critical, as delays can result in an automatic loss.

Key Statistic: Merchants who manage their chargeback processes efficiently and respond within the allotted timeframe have a 60% higher chance of winning disputes.

4. Implement a Strong Prevention Strategy

Preventing chargebacks is the most effective way to reduce their financial and operational burden. A well-rounded prevention strategy should include:

- Clear Payment Terms and Conditions: Ensure that customers understand your refund policy, shipping details, and billing descriptors.

- Use Address Verification Service (AVS): This service matches the billing address provided by the customer with the one on file at the issuing bank, preventing fraudulent transactions.

- Implement 3D Secure (3DS): 3D Secure adds an extra layer of security, requiring customers to verify their identity with a password or PIN, reducing the likelihood of fraudulent charges.

Key Statistic: Chargeback fraud accounts for 70% of the $48 billion in losses merchants are projected to incur due to online payment fraud.

5. Ongoing Training and Development

Utilizing Data in Chargeback Management

- Spot trends and patterns: For example, if you notice a spike in chargebacks during a certain period, you can identify if it is linked to a particular product, region, or customer demographic.

- Improve customer service processes: You can identify common issues that lead to disputes and address them proactively.

- Optimize fraud prevention techniques: Tracking fraudulent chargebacks and their sources can help fine-tune fraud detection systems, reducing future chargeback occurrences.