Accepting credit cards is essential for most businesses today, but the fees can quietly add up. Many merchants assume payment processing rates are fixed, when in reality there is often room to negotiate certain components.

Understanding how processing fees work and knowing what to ask for can significantly reduce costs over time. For businesses processing large volumes, even a small rate reduction can translate into thousands of dollars in savings each year.

In this guide, we’ll break down how payment processing fees work, which parts can actually be negotiated, and the strategies businesses use to lower their rates.

The Real Cost of Payment Processing

When a customer pays with a credit or debit card, the merchant pays a small percentage of the transaction as a processing fee. These fees typically range between 1.5% and 3.5% per transaction, depending on factors like card type, payment method, and the merchant’s industry.

The average total processing cost is about 2.2% per transaction, although it can be higher for premium cards or online transactions.

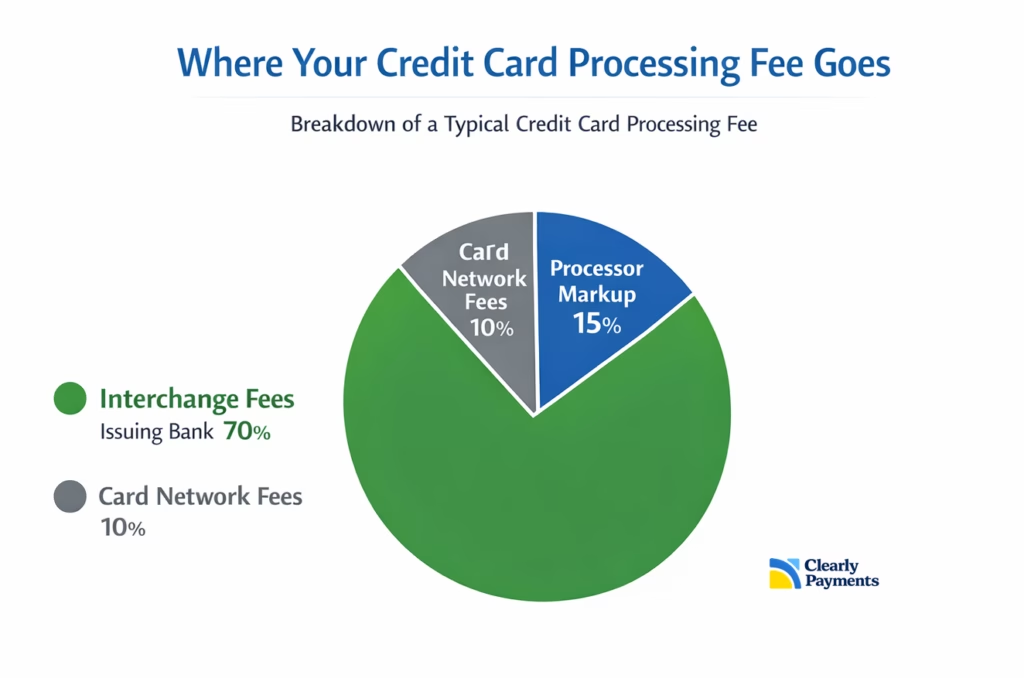

A key point many merchants don’t realize is that most of the fee does not go to the payment processor.

Typical Breakdown of a Credit Card Fee

| Fee Component | Who Receives It | Typical Share |

|---|---|---|

| Interchange Fee | Card issuing bank | 70–90% of total fees |

| Network Assessment | Visa / Mastercard | Small percentage |

| Processor Markup | Payment processor | Negotiable portion |

Interchange fees alone typically represent 70% to 90% of the total cost, making them the largest component of card processing expenses.

Average Processing Fees by Card Type

Different cards cost merchants different amounts to accept. Premium rewards cards typically carry higher interchange fees because they fund consumer rewards programs.

Typical Processing Costs

| Card Type | Typical Merchant Cost |

|---|---|

| Interac Debit | ~0.5% or fixed fee |

| Standard Credit Card | 1.5% – 2.2% |

| Premium Rewards Card | 2.2% – 3.0% |

| Online / Card Not Present | 2.5% – 3.5% |

Debit transactions often carry much lower costs. In some cases the interchange portion can be only a few dozen cents per transaction, depending on the network and processor markup.

Premium credit cards, however, can exceed 2% interchange alone depending on the card tier.

What Parts of Payment Processing Can Be Negotiated?

One of the biggest misconceptions about payment processing is that all fees are fixed. In reality, some parts are controlled by the card networks and issuing banks, while others are determined by the processor.

Fees That Cannot Be Negotiated

These are set by the card networks:

- Interchange fees

- Card network assessment fees

- Regulatory or government mandated fees

These charges are the same regardless of which payment processor you use.

Fees That Can Often Be Negotiated

Merchants can frequently negotiate the following:

- Processor markup percentage

- Per-transaction fee

- Monthly account fee

- PCI compliance fee

- Chargeback handling fee

- Gateway fees for ecommerce

For higher volume merchants, even a 0.10% reduction can produce significant annual savings.

How Much Can Businesses Save?

Small improvements in processing rates can produce meaningful savings for growing businesses.

Example Savings From Rate Negotiation

| Monthly Processing Volume | Rate Reduction | Annual Savings |

|---|---|---|

| $25,000 | 0.20% | $600 |

| $100,000 | 0.20% | $2,400 |

| $250,000 | 0.20% | $6,000 |

| $500,000 | 0.20% | $12,000 |

Because many businesses process hundreds of thousands of dollars in card payments each year, negotiating even small changes can have a noticeable impact on profitability.

7 Ways to Negotiate Payment Processing Rates

Businesses that approach processors with good information and leverage tend to secure the best pricing.

1. Understand Your Current Effective Rate

Before negotiating, calculate your true processing cost.

Look at your statement and divide: Total fees ÷ total card volume

This gives you your effective processing rate.

2. Know Your Processing Profile

Processors price merchants based on risk and transaction patterns.

Helpful metrics include:

- Monthly processing volume

- Average transaction size

- Percentage of online vs in-person transactions

- Chargeback history

A stable profile makes it easier to request better rates.

3. Ask for Interchange-Plus Pricing

Interchange-plus pricing is considered the most transparent model. Instead of a bundled rate, merchants pay: Interchange + processor markup.

Example:

| Component | Example |

|---|---|

| Interchange | 1.65% |

| Processor markup | 0.30% |

| Per transaction | $0.08 |

This structure makes it easier to see exactly what you are paying the processor.

4. Request Removal of Hidden Fees

Many merchant accounts include unnecessary charges.

Common negotiable fees include:

- Monthly statement fee

- PCI compliance fee

- Batch fees

- Minimum monthly fees

Removing these can reduce overall costs even if the percentage rate stays the same.

5. Leverage Competing Quotes

Processors compete aggressively for merchant accounts. Getting multiple quotes often provides negotiating leverage. Businesses can simply say: “Another processor offered a lower markup. Can you match it?”

6. Increase Your Processing Volume

Higher processing volumes often unlock better pricing tiers. Processors prefer merchants who process larger volumes because it spreads operational costs across more transactions.

7. Work With a Transparent Payment Provider

Not all processors structure pricing the same way.

Some providers emphasize transparency by clearly separating interchange, network fees, and processor markup.

This approach helps businesses understand exactly where their payment processing costs come from.

Overall Payment Negotiation

Payment processing fees are a necessary cost of accepting card payments, but that doesn’t mean businesses should accept the first rates they are offered. Many businesses can reduce their payment costs without changing how they accept payments.

Even small reductions can produce significant long-term savings as businesses grow.

For companies processing large transaction volumes, optimizing payment processing rates can be one of the easiest ways to improve margins.